The Wall Street Legal & Regulatory Feed

Securities Industry Commentator by Bill Singer Esq

September 14, 2018

BREAKING NEWS:

U.S. v. Paul J. Manafort, Jr. (1:17-cr-201, District of Columbia)

Paul J. Manafort, Jr. pled guilty in the United States District Court for the District of Columbia to a Superseding Criminal Information, which includes conspiracy against the United States (conspiracy to commit money laundering, tax fraud, failing to file Foreign Bank Account Reports and Violating the Foreign Agents Registration Act, and lying and misrepresenting to the Department of Justice) and conspiracy to obstruct justice (witness tampering). READ the FULL TEXT:

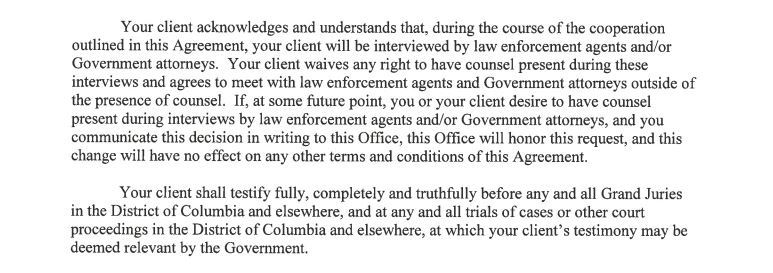

From the "Cooperation" section of the Plea Agreement:

From the Preamble portion of the Information:

1. PAUL J. MANAFORT, JR. (MANAFORT) served for years as a political consultant and lobbyist. Between at least 2006 and 2015, MANAFORT conspired with Richard W. Gates(Gates), Konstantin Kilimnik (Kilimnik), and others to act, and acted, as unregistered agents of a foreign government and political party. Specifically, MANAFORT conspired to act and acted as an agent of the Government of Ukraine, the Party of Regions (a Ukrainian political party whose leader Victor Yanukovych was President from 2010 to 2014), President Yanukovych, and the Opposition Bloc (a successor to the Party of Regions that formed in 2014 when Yanukovych fled to Russia). MANAFORT generated more than 60 million dollars in income as a result of his Ukraine work. In order to hide Ukraine payments from United States authorities, from approximately 2006 through at least 2016, MANAFORT, with the assistance of Gates and Kilimnik, laundered the money through scores of United States and foreign corporations, partnerships, and bank accounts.2. In furtherance of the scheme, MANAFORT funneled millions of dollars in payments into foreign nominee companies and bank accounts, opened by him and his underlings in nominee names and in various foreign countries, including Cyprus, Saint Vincent & the Grenadines (Grenadines), and the United Kingdom. MANAFORT hid the existence of the foreign companies and bank accounts, falsely and repeatedly reporting to his tax preparers and to the United States that he had no foreign bank accounts.3. In furtherance of the scheme, MANAFORT concealed from the United States his work as an agent of, and millions of dollars in payments from, Ukraine and its political parties and leaders. Because MANAFORT directed a campaign to lobby United States officials and the United States media on behalf of the Government of Ukraine, the President of Ukraine, and Ukrainian political parties, he was required by law to report to the United States his work and fees. MANAFORT did not do so, either for himself or any of his companies. Instead, when the Department of Justice sent inquiries to MANAFORT in 2016 about his activities, MANAFORT responded with a series of false and misleading statements.4. In furtherance of the scheme, MANAFORT used his hidden overseas wealth to enjoy a lavish lifestyle in the United States, without paying taxes on that income. MANAFORT, without reporting the income to his bookkeeper or tax preparers or to the United States, spent millions of dollars on luxury goods and services for himself and his extended family through payments wired from offshore nominee accounts to United States vendors. MANAFORT also used these offshore accounts to purchase multi-million dollar properties in the United States. Manafort then borrowed millions of dollars in loans using these properties as collateral, thereby obtaining cash in the United States without reporting and paying taxes on the income. In order to increase the amount of money he could access in the United States, Manafort defrauded the institutions that loaned money on 3 these properties so that they would lend him more money at more favorable rates than he would otherwise be able to obtain.5. Manafort laundered more than $30 million to buy property, goods, and services in the United States, income that he concealed from the United States Treasury, the Department of Justice, and others. MANAFORT cheated the United States out of over $15 million in taxes.

https://www.sec.gov/news/press-release/2018-1911

Convergex Execution Solutions LLC, now known as Cowen Execution Services LLC, will pay $2.75 million to settle SEC charges that the broker-dealer provided incomplete and deficient securities trading information known as "blue sheet data." The SEC Order alleges that from May 1, 2012 to Feb. 28, 2016, approximately 29% of Convergex's submissions contained deficient customer identifying information. Although the Financial Industry Regulatory Authority (FINRA) sanctioned Convergex in March 2012 for deficient blue sheet submissions, the SEC Order found that the firm did not take reasonable steps to ensure that its blue sheet submissions to the SEC contained complete and accurate information and failed to identify the deficiencies during this period. READ the FULL TEXT SEC Order https://www.sec.gov/litigation/admin/2018/34-84116.pdf

A Remark-able Day At the SEC:

Statement Regarding SEC Staff Views (SEC Chairman Jay Clayton)https://www.sec.gov/news/public-statement/statement-clayton-091318SEC Chair Clayton states that public engagement on staff statements and staff documents is important and assists the SEC in developing rules and regulations; however, he admonishes that the SEC and only the SEC adopts rules and regulations that have the force and effect of law. Also see:Remarks to the SEC Investor Advisory Committee by Chairman Jay Clayton

https://www.sec.gov/news/public-statement/statement-clayton-iac-091318https://www.sec.gov/news/public-statement/statement-regarding-staff-proxy-advisory-letters

Four Defendants Sentenced Following Convictions At Trial For Stealing Confidential Government Information And Using It To Engage In Illegal Trading (DOJ Release)

https://www.justice.gov/usao-sdny/pr/four-defendants-sentenced-following-convictions-trial-stealing-confidential-government

https://www.justice.gov/usao-sdny/pr/four-defendants-sentenced-following-convictions-trial-stealing-confidential-government

Federal prosecutors alleged that from at least in or about 2009 through in or about 2014, political intelligence consultant David Blaszczak, Centers for Medicare and Meidcaid Services government employee Chrisotpher Worrall, Deefield management Company, L.P. partners and analysts Theodore Huber, and Robert Olan participated in a scheme to convert to their own use confidential and material nonpublic information from CMS concerning, among other things, CMS's internal deliberations regarding coverage and reimbursement decisions. Following a four-week jury trial in the United States District Court for the Southern District of New York, Blaszczak was found guilty of 10 counts, Huber and Olan of five counts each, and Worrall of two counts. Blaszczak was sentenced to 12 months and one day in prison plus two years of supervised release, including one year of home confinement, and ordered to forfeit $727,500 and pay restitution to CMS in the amount of $1,644.26.Worrall was was sentenced to 20 months in prison plu one year of supervised release, and ordered to pay restitution to CMS in the amount of $1,644.26.Huber and Olan were each sentenced to 36 months in prison plus two years of supervised release, and ordered to forfeit $87,078 and $98,244, respectively, and to each pay restitution to CMS in the amount of $1,644.26, and pay a fine of $1.25 million..

In the Matter of Brett Thomas Graham (SEC Order Denying Request To Modify Settlement Order; '34 Release No. 84106 Invest. Adv. Act Release No. 5005; Invest. Co. Act Release No. 33225; Admin. Proc. File No. 3-16389)

On February 19, 2015, the SEC accepted Brett Thomas Graham's offer of settlement and entered an order that, among other things, barred him from acting in specified capacities in the securities industry with the right to apply for reentry after three years. In that Order, the SEC found that Graham willfully violated Exchange

Act Section 10(b) and Rule 10b-5 thereunder during the course of five liquidation auctions in

2012 and acted knowingly or recklessly. Graham was the Chief Executive Officer of broker-dealer VCAP Securities, LLC, and the managing partner,

Chief Investment Officer, and a portfolio manager of VCAP's affiliated investment adviser,

Vertical Capital, LLC. The Order found that VCAP received nearly $1.2 million in fees, of which

Graham received 10%, for conducting liquidation auctions in which it improperly participated, acquiring 23 securities for nearly $12 million. In response to Graham's motion to vacate portions of its Order imposing certain bars and to waive Rule 506 "Bad Actor" provisions, the SEC Division of Enforcement opposed the motion. The SEC denied the motion largely based upon a finding that Graham failed to show compelling

circumstances that establish it is consistent with the public interest and investor protection to

permit him to function in the industry without the bars he seeks to

vacate. An interesting series of arguments that Graham raised involved his contention that the Supreme Court's 2017 Opinion in Kokesh v. SEC compelled the modification of his Bar on the basis that the sanction was impermissibly both punitive and excessive. In fairly blunt terms, the SEC dismissed the Kokesh line of argument as not applicable. For background, READ SEC "Saad Saga Still Slogs Still Sags" (BrokeAndBroker.com Blog) and "BREAKING NEWS: SEC Loses Supreme Court Kokesh Disgorgement Case" (BrokeAndBroker.com Blog).

Roger Dale Williams Sentenced To 63 Months in Prison for Phony Investment Scheme (DOJ Release)

https://www.justice.gov/usao-edtn/pr/roger-dale-williams-sentenced-63-months-prison-phony-investment-scheme

https://www.justice.gov/usao-edtn/pr/roger-dale-williams-sentenced-63-months-prison-phony-investment-scheme

Roger Dale Williams pled guilty in the United States District Court for the Eastern District of Tennessee to mail fraud and tax charges stemming from his scheme to defraud victims, many who were elderly, who believed that they were investing money in an "investment club" and, later, in church bonds. As pastor of King Branch Road Church of Christ, Williams solicited funds for the purchase of purported church bonds and claimed the funds would be used for the benefit of the church, particularly to pay off the church's debt; howevber, he diverted the funds for his personal use and to make Ponzi-like payments to club members. Williams was sentenced to 63 months in prison and ordered to pay $1,373,361.96 in restitution Many of his victims were elderly. In order to perpetuate the scheme, he also provided victims with false IRS forms pertaining to their purported investments.

Nigerian National Sentenced to 32 Months in Prison for Phishing Scheme That Victimized School Employees (DOJ Release)

https://www.justice.gov/usao-ct/pr/nigerian-national-sentenced-32-months-prison-phishing-scheme-victimized-school-employees

https://www.justice.gov/usao-ct/pr/nigerian-national-sentenced-32-months-prison-phishing-scheme-victimized-school-employees

Adekunle Ojo pled guilty in the United States District Court for the District of Connecticut one count each of conspiracy to commit wire fraud and identity theft in connection with his role in fraudulently obtaining the personal identifying information of school employees and filing 122 false Form 1040 tax returns seeking $596,890 in refunds in the names of those victims. The identity theft was accomplished via an email purporting to be from a schools employee sent to another schools employee seeking W-2 tax information for all system employees. About six returns were processed, and $36,926 in fraudulently-obtained funds were electronically deposited into various bank accounts. Ojo was sentenced to 32 months in prison plus three years supervised release and ordered to pay $36,926 in restitution to the IRS.