The Wall Street Legal & Regulatory Feed

Securities Industry Commentator by Bill Singer Esq

May 18, 2022

FINRA Fines and Suspends Former Morgan Stanley Rep For Putting Compliance Cart After the Horse (BrokeAndBroker.com Blog)

https://www.brokeandbroker.com/6456/finra-awc-zotenko/

At first blush, a recent FINRA AWC seems to be piling it on against a former Morgan Stanley rep over some silliness involving unapproved emails about a private placement offered by the firm. It's not like the rep was pushing an outside deal involving a algorithm-based meme-stock trading program funded by a crypto-mining platform powered by municipal waste. Yeah, I know, where can you get into that hot deal, right? But, getting back to the seemingly beleaguered rep, as it turns out, FINRA was justified in fining and suspending him; and Morgan Stanley may have been on similarly firm ground when it discharged the employee. What could go so horribly wrong? Read today's blog.

Three Portfolio Managers and Allianz Global Investors U.S. Charged in Connection with Multibillion-Dollar Fraud Scheme/ Gregoire Tournant, Chief Investment Officer of Allianz Global Investors U.S.'s Structured Products Group, and Two Others Charged with Fraud Offenses / Allianz Global Investors U.S. LLC Also Charged with Securities Fraud, Agrees to Plead Guilty (DOJ Release)

https://www.justice.gov/opa/pr/three-portfolio-managers-and-allianz-global-investors-us-charged-connection-multibillion

-and-

SEC Charges Allianz Global Investors and Three Former Senior Portfolio Managers with Multibillion Dollar Securities Fraud / Allianz Global Investors Agrees to Pay More Than $1 Billion to Resolve SEC Charges (SEC Release)

https://www.sec.gov/news/press-release/2022-84

https://www.sec.gov/news/press-release/2022-84

An Indictment was unsealed in the United States District Court for the Southern District of New York ("SDNY") charging Gregoire Tournant, the Chief Investment Officer and co-lead Portfolio Manager for a series of private investment funds managed by Allianz Global Investors U.S. LLC ("AGI"), with securities fraud, investment adviser fraud and obstruction of justice offenses in connection with a scheme to defraud investors. Also, Trevor Taylor and Stephen Bond-Nelson pled guilty to Informations filed in SDNY and are cooperating with the government. Pursuant to a Plea AGI will plead guilty to securities fraud in connection with this fraudulent scheme, and pay over $3 billion in restitution, a criminal fine of approximately $2.3 billion, and forfeit approximately $463 million to the government. As alleged in part in the DOJ Release:

Between 2014 and 2020, Gregoire Tournant, the defendant, was the Chief Investment Officer of a set of private funds at AGI known as the Structured Alpha Funds. These funds were marketed largely to institutional investors, including pension funds for workers all across America. As alleged, Tournant and his co-conspirators misled these investors into believing that the funds were protected from a sudden stock market crash with particular hedges. But in late 2015, as the cost of those promised hedges increased, Tournant decided to lie and secretly buy cheaper hedges that provided much less protection to investors. As alleged, Tournant and his co-conspirators also provided investors with altered documents that were sent to investors to hide the true riskiness of the funds' investments, including that they were buying cheaper hedges.In March 2020, following the onset of market dislocations brought on by the COVID-19 pandemic, the funds lost in excess of $7 billion in market value, including over $3.2 billion in principal, faced margin calls and redemption requests, and ultimately were shut down. More than 100 institutional investors, representing more than 100,000 individuals, were victims of this scheme. These institutional investors included, among others, pension funds for teachers in Arkansas, laborers in Alaska, bus drivers and subway conductors in New York City, as well as religious organizations, engineers, and other individuals, universities and charitable organizations across the United States.The scheme alleged was an egregious, long-running and extensive fraud that went undetected for years. It occurred at a very profitable component of AGI - one that accounted for 25% of AGI's revenue in recent years, which amounted to hundreds of millions of dollars. As alleged, one of the ways Tournant carried out the fraud was by marketing the fact that he worked for a well-respected financial institution, AGI, which is a part of the Allianz SE (Allianz) family. Allianz is one of the world's largest financial services companies and one of the world's largest insurance companies. Tournant touted the protections provided by the funds' position within the global Allianz corporate structure, calling Allianz a "master cop" that would ensure that Tournant followed the risk guidelines promised to investors.Despite Tournant's claim that Allianz acted as a "master cop" looking over his shoulder, no one at AGI or Allianz was verifying that Tournant and his colleagues were actually adhering to the investment strategies promised to investors. No risk or compliance personnel at AGI verified, attempted to verify or were responsible for verifying that Tournant and his colleagues were purchasing hedging positions within the range that was represented to investors. Much of this historic fraud was made possible because AGI's control environment was not designed to verify that Tournant and his co-conspirators were telling investors the truth. Because AGI, a registered investment adviser, failed to provide meaningful oversight, Tournant and his co-conspirators were able to deceive investors about the risks they were taking with their money.In addition, as alleged, in the summer of 2020, after the onset of the pandemic and in order to cover up the fraudulent scheme, Tournant attempted to obstruct an investigation by the U.S. Securities and Exchange Commission (SEC) into the circumstances that led to the losses in March 2020.

Defendants reduced losses under a market crash scenario in one risk report sent to investors from negative 42.1505489755747% to negative 4.1505489755747% -- by simply dropping the single digit 2. In another example, defendants "smoothed" performance data sent to investors by reducing losses on one day from negative 18.2607085709004% to negative 9.2607085709004% -- this time by cutting the number 18 in half.When the 2020 COVID-related market volatility revealed that AGI US and the defendants had misled investors about the fund's level of risk, the fund suffered catastrophic losses and investors lost billions; the defendants all the while profited from their deception. The complaint further alleges that Tournant, Taylor, and Bond-Nelson then made multiple, ultimately unsuccessful, efforts to conceal their misconduct from the SEC, including false testimony and meetings in vacant construction sites to discuss sending their assets overseas.. . .

AGI US admitted that its conduct violated the federal securities laws and agreed to a cease-and-desist order, a censure and payment of $315.2 million in disgorgement, $34 million in prejudgment interest, and a $675 million civil penalty, a portion of which will be distributed to certain investors, with the amount of disgorgement and prejudgment interest deemed satisfied by amounts it paid to the U.S. Department of Justice as part of an integrated, global resolution. In a parallel criminal proceeding, the U.S. Attorney's Office for the Southern District of New York today announced criminal charges for similar conduct against AGI US, Tournant, Taylor, and Bond-Nelson. As part of the parallel criminal proceeding, AGI US, Taylor and Bond-Nelson have agreed to guilty pleas.The SEC's complaint seeks permanent injunctions, disgorgement plus interest, and penalties against Tournant, Taylor, and Bond-Nelson. In addition, the complaint seeks an officer and director bar against Tournant. Taylor and Bond-Nelson have agreed to the entry of partial judgments against them in which they consent to injunctive relief with monetary relief to be determined by the court in the future. These settlements are subject to court approval. Taylor and Bond-Nelson also agreed to associational and penny stock bars.As a consequence of the guilty plea, AGI US is automatically and immediately disqualified from providing advisory services to US registered investment funds for the next ten years, and will exit the business of conducting these fund services. To avoid disruptions to these funds and for the protection of the fund investors, the SEC will allow a brief transition period solely to transition these services to another investment adviser. The transition period will be ten weeks for the US mutual funds that AGI US sub-advises and four months for the US closed-end funds that AGI US advises.

READ: The SEC Orders Instituting Proceedings, Making Findings, and Imposing Remedial Sanctions:

- Taylor https://www.sec.gov/litigation/admin/2022/34-94925.pdf

- Bond-Nelson https://www.sec.gov/litigation/admin/2022/34-94926.pdf

- Allianz https://www.sec.gov/litigation/admin/2022/34-94927.pdf

https://www.sec.gov/litigation/litreleases/2022/lr25394.htm

Without admitting or denying the allegations in an SEC Complaint filed in the United States District Court for the Central District of California, attorney Jillian Sidoti consented to the entry of a Final Judgment permanently enjoining her from violating the securities registration and antifraud provisions of Sections 5(a), 5(c), 17(a)(1), and 17(a)(3) of the Securities Act, and the antifraud provisions of Section 10(b) of the Securities Exchange Act and Rule 10b-5 thereunder; and, further, she consented to the imposition of a five-year penny stock bar and a five-year conduct-based injunction that restricts her ability to prepare opinion letters, and to pay a $22,000 civil penalty and just under $14,169 in disgorgement and $4,665 in prejudgment interest. As alleged in part in the SEC Release:

[S]idoti acted as the attorney for penny stock company Blake Insomnia Therapeutics, drafting and signing documents that she knew contained materially false information regarding the operations and control of Blake. Sidoti allegedly then arranged to sell almost all of Blake's stock to multiple nominee shareholders to obscure the fact that the purchasers were a single control group. The complaint further alleges that Sidoti authored opinion letters containing false statements about the control of Blake to induce Blake's transfer agent to remove restrictive legends from its stock certificates, and to induce the Depository Trust Corporation to accept Blake shares for deposit. According to the complaint, Sidoti's actions enabled the control group to evade legal restrictions on the sales of stock by affiliates and sell over five million Blake shares into the public market.

Court Enters Final Judgment Against Investment Adviser COO (SEC Release)

https://www.sec.gov/litigation/litreleases/2022/lr25395.htm

https://www.sec.gov/litigation/litreleases/2022/lr25395.htm

The United States District Court for the Southern District of New York entered a Final Judgment that permanently enjoin Richard T. Diver (the former chief operating officer ("COO") of an investment adviser) from future violations of Sections 206(1) and 206(2) of the Investment Advisers Act of 1940; and holds him liable for $734,558 in disgorgement plus prejudgment interest in the amount of $70,618.53 -- the total of which, $805,176.53, was deemed satisfied by the criminal restitution and forfeiture order entered against Diver in United States v. Richard Diver, 19-cr-533 (S.D.N.Y.). As alleged in part in the SEC Release:

[D]iver stole approximately $6 million from his employer, an investment adviser registered with the Commission. As alleged in the complaint, between 2011 and 2018, Diver, whose duties as the company's COO included managing the company's payroll and client billing, inflated his own pay by approximately $600,000 per year. According to the complaint, Diver misused his position as COO to cause the company to overbill its clients to generate additional revenue so that he could continue financing his inflated salary. As set forth in the complaint, during the course of his fraudulent scheme, Diver caused the company to overbill its clients by approximately $750,000 from over 300 investment advisory client accounts.

CFTC Charges Florida Man and His Two Entities for Operating a $3.4 Million Commodity Futures Fraud (CFTC Release)

https://www.cftc.gov/PressRoom/PressReleases/8531-22

https://www.cftc.gov/PressRoom/PressReleases/8531-22

The CFTC filed a Complaint in the United States District Court for the Southern District of Florida against Damian Castilla and his companies, DCAST Capital Investments LLC and Five Traders LLC,, alleging that from January 2014 through the present, Castilla and his companies defrauded at least 50 pool participants of approximately $3.4 million through commodity pools that purported to trade commodity futures. As alleged in part in the CFTC Release:

[T]he defendants made various material misrepresentations to solicit pool participants, including that they earned significant profits trading futures for pool participants. The defendants' limited futures trading was not profitable, and instead of trading as promised, the defendants misappropriated the vast majority of pool participant funds. They used pool participant funds for car payments, home remodeling, lawn services, clothing, dining, and other personal expenses. The complaint also states that they continued their fraud by issuing false account statements that showed profitable trading in nonexistent trading accounts and by using a portion of the funds obtained from pool participants to pay fake profits to earlier pool participants.

Investor Protection in a Digital Age," Remarks Before the 2022 NASAA Spring Meeting & Public Policy Symposium by Chair Gary Gensler

https://www.sec.gov/news/speech/gensler-remarks-nasaa-spring-meeting-051722

Thank you, Melanie. My thanks to the state securities regulators in the audience and to the North American Securities Administrators Association (NASAA) for your vital work to protect investors.As is customary, I'd like to note that my views are my own, and I'm not speaking on behalf of the Commission or SEC staff.Today, you've asked me to talk about investor protection in a digital age.The topic gets me thinking about grocery stores.When you visit a grocery store, do you notice that you travel around the outer aisles to find the fruits and vegetables, but the candy, gum, and chips are waiting for you near the cash register?By design, grocery stores tap into our behavioral psychology, activating our impulses to purchase things we may not need. Research has shown that impulsive purchases account for 62% of supermarket sales.[1] A bit of evidence: all those bags of gummy bears I've purchased in my day.These stores serve the public, and they also have a profit incentive. Thus, they may tempt us with products that serve their interests rather than ours, and use the latest technology and research to do so.[2] Many consumers recognize this.When instead we seek advice from an investment professional, that expectation changes. If you are a broker-dealer or an investment adviser-including if you provide your services digitally through an investment platform-when you provide advice, you have to act in the best interests of us, your clients, and not place your own interests ahead of our interests.[3]As my mom, Jane Gensler, might have said it, you have to put your client's interests first. You can't dangle gummy bears over an investor's shopping cart, so to speak-even if the latest technologies might make it all the more easy, subtle, and profitable to do so.My mom would have been right, because there's something distinctive about finance. Investment professionals are dealing with other people's money. That's why brokers and advisers have to comply with specific duties-standards on care, loyalty, best interest, and best execution.The challenge is to make sure that brokers and advisers live up to their obligations and the trust that's been placed in them.This challenge is not new, nor is the digital age.The technological advances of the 1990s, namely the internet, allowed anyone to execute a transaction online. Among other factors, that shift created further incentives for brokers to restyle themselves as advisers.[4]By the naughts, investors found it difficult to see the difference between brokers and advisers, the services they offer, and the disparate standards required of those professionals.[5] After smartphones came around, investors might have started to believe that the difference between brokers and advisers might merely be tapping one part of their screen versus another.In 2019, the SEC addressed this blurring and these disparities through rulemaking on Regulation Best Interest (Reg BI) for broker-dealers and through an interpretation of the fiduciary standard for investment advisers (IA fiduciary standard). [6] These set forth in clear terms the responsibilities that these investment professionals owe to investors when providing advice.These responsibilities matter for tens of millions of investors. Think about them: the college graduate paying off her student loans; the parents-in-waiting saving for that new house with a crib; the grandparents living off their nest egg.Our current digital age of the 2020s raises additional challenges for investors. It's dangling over their shopping carts. Through new technologies, investors-who at the time might not even be seeking advice-may be getting nudged toward those gummy bears.Digital Engagement PracticesI think what we're living through in the 2020s is as transformative as the 1990s was with the internet. What I'm referencing is the use of predictive data analytics, built upon artificial intelligence and machine learning, tapping into the veritable explosion of data on every one of us.Coupled with differential marketing, differential pricing, and individually tailored behavioral prompts, these technologies-what we've called digital engagement practices (DEPs)-are increasingly shaping many parts of our economy.Conflicts of InterestFinance is no exception. Predictive data analytics and other DEPs are evolving the way that brokers and advisers engage with investors, including through robo-advisers, brokerage apps, and wealth management apps.[7]As a thought experiment, imagine if the grocery store were a virtual experience. Imagine if the store rearranged its inventory, shelving, and pricing for each shopper who visited the store, each time they visited that store, down to the impulse items by the register. The precision with which the store could nudge you toward certain purchases-and the algorithms behind those nudges-could be powerful and profitable.That thought experiment may not have fully come to finance yet. Through using DEPs, however, robo-advisers, brokerage apps, and wealth management apps increasingly can narrowly target each consumer with specific marketing, pricing, and nudges.This raises a number of questions. In the case of online investment platforms, when they use certain DEPs, what are they optimizing for? Are they optimizing for the investor's benefits, including risk appetite and returns? Or are they prioritizing other factors, including the platform's revenue or performance?When investment professionals offer advice or recommendations, including when they are using DEPs, our standards are clear-they must not place their own interests ahead of the investor's interests.[8]This new digital world raises questions. Is a behavioral nudge-the gummy bears dangled above your cart, the flashing "options trading" button when you create a brokerage account-a recommendation?Further, when do behavioral nudges take on attributes similar enough to advice or recommendations such that related investor protections are needed? The nature of certain steers raises questions between what is and isn't advice or a recommendation.BiasA related issue is bias, and how people-regardless of race, color, religion, national origin, sex, age, disability, and other factors-receive fair access and prices in the financial markets.[9]How can we help ensure that new developments in analytics don't instead reinforce societal inequities?The underlying data used in these analytic models could be based upon data that reflects historical biases, along with underlying features that may be proxies for protected characteristics, like race and gender.As investment platforms rely on increasingly sophisticated data analytics, I believe that it will be appropriate to safeguard against algorithmically fortifying such biases.Systemic Risk-ConcentrationFurther, today's new forms of predictive data analytics raise issues for financial stability through herding, interconnectedness, and possible greater concentration in our capital markets.With respect to concentration, we have seen that sophisticated data analytics-and what's called network economics-have led to highly-concentrated platforms in a range of sectors. For example, last year, 92% of internet searches were logged on a single search platform.[10]Today, though we still see significant competition on the front-end among brokerage apps, there is less so on the back-end.More specifically, the provision of market making by wholesalers, paying for order flow, has already become relatively concentrated. For example, during GameStop events last year, 88% of internalized dollar volume in January 2021 was executed by three wholesalers.[11]To protect investors in a digital age and best promote competition, what might we do if and as greater concentration emerges in finance? We've also seen growing concentration in the investment management field.Generally speaking, the narrower and more concentrated a particular part of the market, the less robust the competition. Thus, I've asked staff to examine how to improve efficiency and competition throughout our markets.Best InterestUnder Reg BI and the IA fiduciary standard, when a broker or an adviser provides advice, digitally or otherwise, they must act in the best interests of their clients, and not place their own interests ahead of their clients' interests.[12]These words matter to investors. They should have meaning for brokers and advisers as well. Thus, I've asked our Divisions of Investment Management, Trading and Markets, Examinations, and Enforcement to help ensure that investment professionals live up to these obligations.The SEC staff published a bulletin in March regarding Reg BI and the IA fiduciary standard. The bulletin addressed account recommendations, including rollover recommendations, and focused on three core points.[13]First, brokers and advisers need to prevent their own interests from inappropriately influencing their recommendations and advice. If they can't do that, they have decisions to make-eliminate the conflict, don't give the advice, or find some other way to ensure that they don't put their interests ahead of the retail investor's interests.Second, in order to offer recommendations and advice in the best interest of the investor, brokers and advisers need to consider reasonably-available alternatives. This needs to be a meaningful evaluation.Third, as part of that analysis, brokers and advisers need to consider costs and risks to investors. While it is true that they don't always have to recommend the lowest-cost option, they must have a reasonable basis to believe a higher-cost recommendation nonetheless is in the investor's best interests.The staff is considering additional bulletins that would further provide their views on each of these three points.Brokers and advisers have a critical role to play in all of this. Disclosure is important but not sufficient when it comes to acting in a retail investor's best interest. Firms need to take investor protection and compliance obligations seriously, reining in or curing any conflicts and really delivering the best interest advice that investors so need and deserve.That's how we get the best out of best interest.Crypto MarketsDiscussing investor protection in a digital age, I'd be remiss not saying a few words on the crypto markets. I'm reminded of Joseph Dolley, the Kansas Banking Commissioner who pioneered investor protection.[14]Over the past year, several bank executives have shared their concerns with me about the sheer number of depositors who have moved money from their bank accounts into crypto-related exchanges and wallets.When I first heard this, I remembered Mr. Dolley's story from a century ago. As banking commissioner, Mr. Dolley heard similar stories from local bank executives. People were withdrawing money from their bank accounts to purchase securities from hucksters and scammers across the state. Mr. Dolley knew something had to be done.His calls for investor protection led to blue-sky laws across many states. This led to the founding of NASAA in 1919. All of this happened in an earlier era of rapidly-changing technology.As I hear from bank executives about their customers shifting their savings to speculative crypto assets, I think of how Mr. Dolley responded to a clear need to protect investors as technology and finance changed.I think there's a need to bring greater investor protection to these crypto markets. Central to that are crypto trading and lending platforms, where investors buy, sell, and lend around $100 billion of crypto assets a day.[15]As it relates to crypto tokens, if investors are putting money behind a group of entrepreneurs raising money from the public in anticipation of profits, that's the hallmark of an investment contract or a security under our jurisdiction.The crypto-related events in recent weeks have highlighted yet again how important it is to protect investors in this highly speculative asset class.ConclusionIn conclusion, when new technologies comes along, the need for investor protection doesn't go away. It comes down to what my mom might have said. You can't simply dangle gummy bears . . . or crypto tokens. . . over an investor's shopping cart.You have to put your client's interests first.Thank you.[1] See Journal of Retailing and Consumer Services, "Impulsive Purchasing in Grocery Shopping: Do the Shopping Companions Matter?" (May 2021), available at https://www.sciencedirect.com/science/article/abs/pii/S0969698921000618.[2] See Institute of Electrical and Electronics Engineers, "The Impacts of E-Payment System and Impulsive Buying to Purchase Intention in E-commerce" (Oct. 2, 2020), available at https://ieeexplore.ieee.org/document/9211154.[3] See U.S. Securities and Exchange Commission, "Regulation Best Interest: The Broker-Dealer Standard of Conduct" (Sept. 10, 2019), available at https://www.sec.gov/rules/final/2019/34-86031.pdf. See U.S. Securities and Exchange Commission, "Commission Interpretation Regarding Standard of Conduct for Investment Advisers" (Jul. 12, 2019), available at https://www.sec.gov/rules/interp/2019/ia-5248.pdf. See U.S. Securities and Exchange Commission, "Regulation Best Interest, Form CRS and Related Interpretations" (March 30, 2022), available at https://www.sec.gov/regulation-best-interest. See U.S. Securities and Exchange Commission Staff, "Staff Bulletin: Standards of Conduct for Broker-Dealers and Investment Advisers Account Recommendations for Retail Investors" (March 30, 2022), available at https://www.sec.gov/tm/iabd-staff-bulletin.[4] See U.S. Securities and Exchange Commission, "Study on Investment Advisers and Broker-Dealers" (Jan. 2011), available at https://www.sec.gov/news/studies/2011/913studyfinal.pdf. See The Rand Institute for Civil Justice, "Investor and Industry Perspectives on Investment Advisers and Broker-Dealers" (Jan. 2008), available at https://www.sec.gov/news/press/2008/2008-1_randiabdreport.pdf.[5] See U.S. Securities and Exchange Commission, "Study on Investment Advisers and Broker-Dealers" (Jan. 2011), available at https://www.sec.gov/news/studies/2011/913studyfinal.pdf. See U.S. Securities and Exchange Commission, "Investor and Industry Perspectives on Investment Advisers and Broker-Dealers" (Jan. 2008), available at https://www.sec.gov/news/press/2008/2008-1_randiabdreport.pdf.[6] See Footnote 3. See also U.S. Securities and Exchange Commission, "Regulation Best Interest, Form CRS and Related Interpretations" (March 30, 2022), available at https://www.sec.gov/regulation-best-interest.[7] See Gary Gensler, "Prepared Remarks before the Investor Advisory Committee" (March 10, 2022), available at https://www.sec.gov/news/statement/gensler-iac-2022-03-10.[8] See Footnote 3.[9] See Gary Gensler, "Prepared Remarks before the Investor Advisory Committee" (March 10, 2022), available at https://www.sec.gov/news/statement/gensler-iac-2022-03-10. See Gary Gensler, "Prepared Remarks at SEC Speaks" (Oct. 12, 2021), available at https://www.sec.gov/news/speech/gensler-sec-speaks-2021-10-12.[10] See StatCounter, available at https://gs.statcounter.com/search-engine-market-share.[11] See U.S. Securities and Exchange Commission Staff, "Staff Report on Equity and Options Market Structure Conditions in Early 2021" (Oct. 14, 2021), available at https://www.sec.gov/files/staff-report-equity-options-market-struction-conditions-early-2021.pdf.[12] See Footnote 3.[13] See U.S. Securities and Exchange Commission Staff, "Staff Bulletin: Standards of Conduct for Broker-Dealers and Investment Advisers Account Recommendations for Retail Investors" (March 30, 2022), available at https://www.sec.gov/tm/iabd-staff-bulletin.[14] See"Kansas Blue Sky Laws,"available athttps://www.kshs.org/kansapedia/kansas-blue-sky-laws/18618.[15] See Gary Gensler, "Prepared Remarks of Gary Gensler on Crypto Markets at the Penn Law Markets Association Annual Conference" (April 4, 2022), available at https://www.sec.gov/news/speech/gensler-remarks-crypto-markets-040422.

Testimony at Hearing before the Subcommittee on Financial Services and General Government U.S. House Appropriations Committee by SEC Chair Gary Gensler

https://www.sec.gov/news/testimony/gensler-testimony-fsgg-subcommittee

https://www.sec.gov/news/testimony/gensler-testimony-fsgg-subcommittee

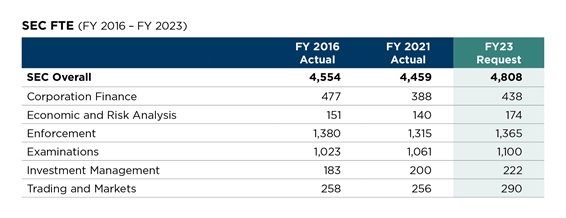

Good morning, Chairman Quigley, Ranking Member Womack, and members of the Subcommittee. I'm honored to appear before you for the second time as Chair of the Securities and Exchange Commission. It is good to be here alongside Federal Trade Commission Chair Khan. As is customary, I'd like to note that my views are my own, and I am not speaking on behalf of my fellow Commissioners or the SEC staff.The Gold Standard of Capital MarketsI'd like to open by discussing two key years in economic policymaking: 1933 and 1934.We were in the midst of the Great Depression. President Franklin Delano Roosevelt and Congress addressed this crisis through a number of landmark policies.Amongst them, in 1933 and 1934, Congress and FDR came together to craft the first two federal securities laws. These statutes created requirements and regulations around disclosure, registration, exchanges, and broker-dealers, and established the SEC to oversee the markets.Additionally, in 1933, President Roosevelt formally suspended the use of the gold standard.[1] Then, in 1934, the Gold Reserve Act was enacted, prohibiting government and financial institutions from redeeming dollars for gold.[1]Though it takes constant vigilance to protect investors, maintain fair, orderly and efficient markets, and facilitate capital formation, the U.S. laws became the gold standard for capital markets around the world.In other words, in those two key years, one could say we replaced one gold standard with another gold standard: the securities laws.The core principles of the securities markets laid out in these statutes were important for issuers and investors in our domestic markets. I believe they also contributed to America's geopolitical standing around the globe.We are blessed with the largest and most innovative capital markets in the world. The U.S. capital markets represent 38 percent of the globe's capital markets.[1] This exceeds even our impact on the world's gross domestic product, where we hold a 24 percent share.What's more, U.S. market participants rely on capital markets more than market participants in any other country. For example, debt capital markets account for 80 percent of financing for non-financial corporations in the U.S. In the rest of the world, by contrast, nearly 80 percent of lending to such firms comes from banks.[2]We are the destination of choice for companies seeking to raise money in both public and private markets. Private capital markets, such as venture capital, have brought new ideas to market quickly and flexibly.We can't take our leadership in capital markets for granted, though.New financial technologies and business models continue to change the face of finance for investors and issuers. More retail investors than ever are accessing our markets. Other countries are developing deep, competitive capital markets as well, seeking to surpass ours.Further, market participant incentives, economic cycles, and the nature of finance itself will constantly challenge even a gold standard. In recent years, we've seen as much - whether the market events of March 2020, the meme stock-related volatility in early 2021, the speculative crypto markets, the boom of special purpose acquisition companies (SPACs), or the collapse of Archegos Capital Management, which we recently charged with fraud and market manipulation.What's more, we are in the midst of uncertain geopolitical events. On top of that, around the globe, central banks have started to transition from an accommodating to a tightening policy stance.Given these trends, I think we should do everything we can to maintain and enhance that gold standard of the markets.Maintaining the Gold StandardThere are two broad ways to do that, in my view.One is to work with the Commission and staff to update our rules for modern markets and technologies as we execute our mission: to protect investors, maintain fair, orderly, and efficient markets, and facilitate capital formation. We must remain vigilant to opportunities to enhance competition, transparency, fairness, and resiliency.The other way - and the main focus of today's testimony - is to ensure that the SEC is adequately resourced so we can remain the cop on the beat. The SEC is deficit-neutral, fully funding ourselves with fees on securities transactions.Having worked in finance for decades, I'd long respected the SEC and its tremendous staff. What I couldn't fully appreciate is the sheer magnitude of this agency's work on a daily basis.We oversee 24 national securities exchanges, 99 alternative trading systems, nine credit rating agencies, seven active registered clearing agencies, five self-regulatory organizations and other external entities. We look after the accounting and auditing functions of the public markets, process thousands of periodic filings and registration statements, and work through thousands of examinations and enforcement actions each year. We review the disclosures and financial statements of more than 8,200 reporting companies.Markets don't stand still. The world isn't standing still. Our resources can't stand still, either.And yet, as I will detail, our agency has shrunk. When I testified you last year, the agency had 4 percent fewer staff than it did in 2016; it remains modestly below where it was in 2016. We can't shrink when we're trying to maintain a gold standard. The best athletes in the world still practice - generally, even more than their competitors.Our capital markets are a national treasure. We, at the SEC, must work to maintain them as the envy of the world. But we can't do it alone. We need the help of Congress.Growth in the MarketsThe last five years have been a remarkable time in our $100-trillion capital markets. Thus, while there are many measures of market activity, by most objective measures, we should have grown during the past five years.Instead, the opposite has happened. As our capital markets have grown, this agency has shrunk.As just a few examples:In the past five years, the number of registered entities we oversee has grown by 12 percent (from 26,000 to 29,000), even though the SEC has shrunk in that time.Since 2016, the number of private funds managed by registered investment advisers has increased 40 percent, to 50,000.The amount of data that the SEC processes has swelled by 20 percent annually for each of the last two years.Moreover, the highly volatile and speculative crypto marketplace has mushroomed, attracting tens of millions of American investors and traders.[3] In 2016, there were an estimated 644 crypto tokens on the worldwide market. Five years later, that number had gone up more than tenfold.[4] The volatility in the crypto markets in recent weeks highlights the risks to the investing public.Technology is rapidly changing as well. Predictive data analytics, including machine learning, are increasingly being adopted in finance - from trading, to asset management, to risk management.[5] Growing cybersecurity risks have implications for the financial sector, investors, issuers, and the economy at large.[6]Beyond that, our responsibilities have grown. Important legislation, such as the Holding Foreign Companies Accountable Act of 2020 (HFCAA), has placed additional demands on our resources. Rules implementing certain mandates of the Dodd-Frank Act of 2010 recently went into effect. Such mandates, designed to protect investors, often have been unfunded.Thus, I am pleased to support the President's Fiscal Year 2023 (FY23) budget request for SEC operations, totaling $2.149 billion, an 8 percent increase over FY22. This request would allow us to maintain current services, add full-time equivalents in critical growth areas, and devote more resources to technology. This number would support a modest growth of (about 6 percent) in full-time equivalents (FTEs) above our previous peak in FY16, assuming consistent vacancy rates.Figure 1: Headcount (FTEs) at the SEC and in individual Divisions. Overall SEC headcount includes all Offices and Divisions.This increase would be modest, given the major trends affecting our markets since 2016. Moreover, to fund our operations, the agency collects fees on securities transactions at a rate intended to fully offset our appropriation.Thanks to the work of the remarkable staff, the SEC has faced the challenges of limited resources well.For the SEC to continue to succeed in carrying out our mission, our personnel level must continue to grow commensurate with the expansion and complexity in the capital markets around the globe.This is not a time to scrimp on the SEC's resources.The SEC has 30 Divisions and Offices across our 11 regional locations and Washington, D.C., headquarters. In the interest of time, I will focus the bulk of this testimony on our six Divisions:

- The Divisions of Enforcement and Examinations, our cops on the beat and eyes and ears on the ground;

- The programmatic Divisions of Corporation Finance, Trading and Markets, and Investment Management; and

- The Division of Economic Risk and Analysis, whose economic analysis undergirds all of our work.

I also briefly will discuss the technology budget at the agency and separate appropriations for the SEC's new headquarters.Budget Request: Enforcement and ExaminationsThe Divisions of Enforcement and Examinations account for about half of the SEC's staff. Without examination against and enforcement of our rules and laws, we can't instill the trust necessary for our markets to thrive. Stamping out fraud, manipulation, and abuse lowers risk in the system. It protects investors and reduces the cost of capital. The whole economy benefits from that.[7]EnforcementThe Division of Enforcement shrank 5 percent from FY16 to FY21. The FTEs level supported by the FY23 budget request would still be 1 percent shy of where we were in 2016.About a quarter of the SEC's staff work in our Division of Enforcement.The Division continues to serve as the cops on the beat of the capital markets, though the demands on their resources has grown.Last year, Enforcement filed about 700 total actions. We also had a record year for our whistleblower program, awarding $564 million to 108 whistleblowers,[8] compared to 39 whistleblowers in FY20.[9] The Office of the Whistleblower received and processed more than 12,000 tips, complaints, and referrals - up nearly threefold over the previous five years.[10] Further, in FY21, we received 46,000 tips, complaints, and referrals from members of the public, up from about 16,000 five years earlier.[11]After peaking in 2016, the last three fiscal years, the Division opened, on average, 1,100 matters under inquiry and investigations. At any given time, we have approximately 1,700 open matters. Our resources may be constrained here. Additional resources will help us keep up with the increasing workload.Beyond that, more cases are being litigated and going to trial. We expect the number of litigated cases to continue to rise as Enforcement increasingly holds wrongdoers accountable with meaningful and, in some instances, escalating sanctions.Moreover, various market events, including the effects of the pandemic, the market volatility in early 2021, and recent events in Ukraine, have placed significant stress on Enforcement resources.Meanwhile, misconduct in emerging and new areas, from complex securities products to new financial technologies to crypto, requires new tools and expertise.The additional staff will provide the Division with more capacity to investigate misconduct and accelerate enforcement actions. It also will strengthen our litigation support, bolster the capabilities of the Crypto Assets and Cyber Unit, and investigate the tens of thousands of tips, complaints, and referrals we receive from the public.ExaminationsThe Division of Examinations has grown modestly (4 percent) since FY16. The FY23 budget request would support an additional 4 percent increase in FTEs compared with FY21.About another quarter of the staff works in our Division of Examinations. This Division serves as the eyes and ears of the Commission, conducting about 3,000 exams per year, compared with 2,427 in 2016.In part, we've maintained this level of productivity because we're doing remote exams due to the pandemic. There's no replacement for on-site exams, though. As registrants are coming back, we will need to factor in additional resources for our Examinations Division to conduct on-site exams.Given the evolving markets, heightened geopolitical environment, and increased attention paid to cyber risks, I expect the demands on Examinations to continue to grow.Since 2016, the number of registered investment advisers has increased 25 percent, to 15,000. This growth directly affects our work. Unlike many other aspects of the markets, including broker-dealers, investment advisers do not have a self-regulatory organization. Thus, the Division of Examinations is the only entity conducting exams of SEC-registered investment advisers.We examined about 15 percent of advisers registered with the SEC in FY20 and FY21. The funds we requested will support only about a 5 percent increase in the number of staff that examine investment advisers.The Division also needs to increase its capacity to examine broker-dealers, particularly when it comes to compliance with Regulation Best Interest.Furthermore, last year, security-based swap dealers and major security-based swap participants were required to register with the Commission for the first time. The Division has begun standing up a team to examine them and to spot risks and issues.Budget Request: Programmatic DivisionsNext, I will turn to our three programmatic Divisions.Corporation FinanceThe Division of Corporation Finance has shrunk 19 percent since 2016. The FY23 budget request would still leave us 8 percent shy of the number of FTEs we had in FY16.The Division oversees the disclosures of registered issuers so that investors have the material information they need to make informed investment decisions. Like other Divisions, their responsibilities have grown in recent years.In FY16, Corporation Finance reviewed filings related to approximately 510 new registrants. That grew almost fourfold last year, to 1,960. Initial public offerings create new disclosures and ongoing streams of work for which SEC staff are responsible. Our role in protecting investors is heightened when a company is being introduced to public investors for the first time.And yet, during that time, the staff of the Division fell. The Division's ability to review filings of existing registrants is more limited given transaction volume and complexity of deals.Furthermore, the Division has sought enhanced disclosures from China-based variable interest entities so that they fully represent the risks of these structures to investors in U.S. capital markets. Recent developments in China, along with the implementation of the HFCAA, have placed additional demands across the Division.[12]Trading and MarketsThe Division of Trading and Markets has shrunk 1 percent since FY16. The FY23 budget request would support a 12 percent increase in FTEs compared with FY16.The Division serves as the front lines for maintaining fair, orderly, and efficient markets. From FY16 to FY21, the size of the Division was basically flat, in terms of FTEs, even as there have been dramatic changes in technology, increased retail participation, and greater volume in the markets.For instance, the average daily number of transactions in equity markets was 35 million in 2016. In 2021, that number had nearly doubled, to 69 million per day.In addition, Trading and Markets reviews thousands of proposed rule changes and advance notices filed by self-regulatory organizations.Investment ManagementThe Division of Investment Management grew 9 percent since FY16 because of the creation of an Analytics Office within that Division; without this new important function, this Division would have shrunk. The FY23 budget request would support FTE levels of 10 percent above FY21.The Division oversees the investment companies and advisers stewarding the nest eggs for millions of American investors.In the past five years, the Division has overseen 50 percent growth (from $67 trillion to $100 trillion) in combined assets under management in registered investment companies, private funds, and separately managed accounts.[13] These sums include the life savings of more than 106 million American investors (an increase of 14 percent from 2016).[14]As the asset management field has grown dramatically in recent years through the rise of 401ks and target-date funds, the demands placed on this key Division have increased even more rapidly, with innovative filings proliferating in particular.Since 2016, the number of registered investment advisers has increased 25 percent, from 12,000 to 15,000. The number of clients for RIAs has expanded 70 percent, from 32 million in 2016 to 55 million in 2021.[15] This is due to the dramatic growth in robo-advisers and other firms that use algorithms and models to provide investment advice directly to investors through separately managed accounts rather than through investment funds.Since 2016, the number of ETFs has increased by 25 percent to roughly 2,300. The amount of assets has more than doubled in that time, to $5.5 trillion.[16] Interest in these financial innovations is driven largely by retail investors and their advisers, so each of those fund filings is reviewed by the Division's disclosure review team.Further, this Division oversees private fund advisers - including private equity fund and venture capital fund advisers - which represent more than $21 trillion in gross assets, a 75 percent increase from 2016.[17] From 2016 to 2021, the number of private funds managed by registered investment advisers has increased 40 percent, to 50,000.[18]Additionally, filings across the board are becoming increasingly complex, reflecting asset growth in innovative areas like crypto, thematic index funds, and Environmental, Social, and Governance. In 2021, 45 filings referred to crypto in their summary prospectuses, up from 6 filings just two years earlier.Budget Request: Three Other AreasBefore I conclude, I will discuss three other topics.Economic Risk and AnalysisThe Division of Economic Risk and Analysis has shrunk 7 percent since FY16. The FY23 budget request would support a 15 percent increase in FTEs compared with FY16.This Division shapes every aspect of our policymaking, from the early design phase to the proposing releases to the consideration of public comments to the adopting releases. It helps us determine the size of fines for enforcement actions. It provides important context for every one of our meetings.TechnologyNext, when it comes to technology, we live in transformational times. The amount of data that the SEC processes has grown by 20 percent annually for the past two years. Further, cyber threats have placed our financial sector on high alert. As technologies evolve, it is important that the SEC's information technology follows suit.We continue to need additional resources to support the Commission's data, cybersecurity, and other IT needs. While our $370 million request for the Office of Information Technology is basically flat with the last two years of spending, in real terms it is up only modestly from FY16. Moreover, for comparison's sake, JPMorgan spends an average of $1 billion in technology each month.[19]It is critical that the SEC have additional technological resources to incorporate analytics and machine learning capabilities for our oversight and surveillance functions, protect agency and registrant information, provide data to the investing public, and much more.HeadquartersThe General Services Administration (GSA) also recently secured a new lease to move the SEC headquarters in Washington to another building. The separate FY23 request of $57.4 million would support GSA's work on the building construction and move-related costs. As requested in the past, the SEC proposes to offset these costs with fee collections and return any unused amounts to fee payers or the Treasury after project completion.ConclusionA year into this role, I remain deeply grateful for the opportunity to work with this remarkable staff and my fellow Commissioners to help maintain American capital markets as the best in the world.As we continue to navigate geopolitical challenges, we must always think about ways to enhance the efficiency, resiliency, and transparency of our markets. What additional resources do we need? Which new rules of the road might we need to meet the promise of our modern markets?The sheer growth and added complexity in the capital markets continue to necessitate greater resources for the SEC.In considering how best to maintain the world's best markets in the 2020s and the 2030s, I can't help but think about the establishment of the federal securities regime in the 1930s. These foundational laws help us maintain our extraordinary competitiveness on the world stage. They are the gold standard. Let's do everything we can to keep them that way in the future.[1] See Securities Industry and Financial Markets Association, "2021 SIFMA Capital Markets Fact Book" (July 2021), available at https://www.sifma.org/wp-content/uploads/2021/07/CM-Fact-Book-2021-SIFMA.pdf.[2] See World Bank data: https://data.worldbank.org/indicator/NY.GDP.MKTP.CD.[3] See Andrew Perrin/Pew Research Center, "16% of Americans say they have ever invested in, traded or used cryptocurrency" (Nov. 11, 2021), available at https://www.pewresearch.org/fact-tank/2021/11/11/16-of-americans-say-they-have-ever-invested-in-traded-or-used-cryptocurrency/.[4] See Statista, "Number of cryptocurrencies worldwide from 2013 to February 2022," available at https://www.statista.com/statistics/863917/number-crypto-coins-tokens.[5] See Gary Gensler, "Prepared Remarks at DC Fintech Week" (Oct. 21, 2021), available at https://www.sec.gov/news/speech/gensler-dc-fintech-2021-10-21.[6] See Gary Gensler, "Cybersecurity and Securities Laws" (Jan. 24, 2022), available at https://www.sec.gov/news/speech/gensler-cybersecurity-and-securities-laws-20220124.[7] See Gary Gensler, "Prepared Remarks at the Securities Enforcement Forum" (Nov. 4, 2021), available at https://www.sec.gov/news/speech/gensler-securities-enforcement-forum-20211104.[8] See "SEC Announces Enforcement Results for FY 2021" (Nov. 18, 2021), available at https://www.sec.gov/news/press-release/2021-238.[9] See "SEC Division of Enforcement Publishes Annual Report for Fiscal Year 2020" (Nov. 2020), available at https://www.sec.gov/news/press-release/2020-274[10] See "Whistleblower Program: 2021 Annual Report to Congress" (p. 28), available at https://www.sec.gov/files/owb-2021-annual-report.pdf.[11] See "Fiscal Year 2023 Congressional Budget Justification, Annual Performance Plan; Fiscal Year 2021 Annual Performance Report" (p. 25), available at https://www.sec.gov/files/FY%202023%20Congressional%20Budget%20Justification%20Annual%20Performance%20Plan_FINAL.pdf, and "Division of Enforcement: 2020 Annual Report" (p. 19) https://www.sec.gov/files/enforcement-annual-report-2020.pdf and "Division of Enforcement: Annual Report - A Look Back at Fiscal Year 2017" (p. 2), available at https://www.sec.gov/files/enforcement-annual-report-2017.pdf.[12] See Gary Gensler, "Statement on Investor Protection Related to Recent Developments in China" (July 30, 2021), available at https://www.sec.gov/news/public-statement/gensler-2021-07-30.[13] Assets in registered investment companies grew from $18.1 trillion in 2016 to $29.7 trillion in 2021. See Investment Company Institute, "2016 Investment Company Fact Book," available at https://www.ici.org/doc-server/pdf%3A2016_factbook.pdf, and "2021 Investment Company Fact Book," available at https://www.ici.org/system/files/2021-05/2021_factbook.pdf ). Assets in private funds grew from $8.7 trillion in 2016 to $21 trillion in 2021 (based on data reported on Form ADV, Schedule D, Section 7.B.1 in 2016 & 2021); and assets in separately managed accounts grew from $40 trillion in 2016 to $49.6 trillion in 2021 (based on data reported on Form ADV, Item 5.D. in 2016 & 2021). The Form ADV data consist of assets that are reported by both advisers and sub-advisers.[14] See "2016 Investment Company Fact Book" and "2021 Investment Company Fact Book."[15] Based on analysis of data reported on Form ADV, Item 5.D. in 2016 and 2021. The data consist of clients that are reported by both advisers and sub-advisers.[16] See Investment Company Institute, "2021 Investment Company Fact Book," available at https://www.ici.org/system/files/2021-05/2021_factbook.pdf.[17] Based on analysis of data reported on Form ADV in 2016 and 2021.The data consist of private funds that are reported by both advisers and sub-advisers.[18] Id.[19] See JPMorgan Chase & Co., "This $12 Billion Tech Investment Could Disrupt Banking," available at https://www.jpmorganchase.com/news-stories/tech-investment-could-disrupt-banking.

Nominee for Upcoming FINRA Board of Governors Election / Petitions for Candidacy Due: Thursday, June 30, 2022 (FINRA Election Notice)

https://www.finra.org/sites/default/files/2022-05/Election-Notice-051622.pdf

At FINRA's annual meeting on August 19, 2022, one Large Firm Governor and one Small Firm Governor will be elected. The FINRA Nominating & Governance Committee ("Nominating Committee") nominated Christopher W. Flint, President, Farmers New World Life, Inc./ Farmers Financial Solutions LLC for the Large Firm Governor vacancy. The Election Notice advises that:

With respect to the Small Firm Governor seat, the Nominating Committee determined it would not nominate a candidate for election in 2022. Instead, any eligible individuals who obtain the requisite number of valid petitions will be certified as candidates and included on the ballot.

Bill Singer's Comment:

In recent years, with the noted exceptions of former Small Firm Governor Stephen A. Kohn and current Small Firm Governor Paige W. Pierce, few Governors (elected or appointed) demonstrated any zealous advocacy on behalf of the investing public and beleaguered Small Firm community. Charged with implementing effective investor protection while ensuring that the legitimate needs of the industry are addressed, the lackluster FINRA Board of Governors has miserably failed on both fronts. Sadly, as the Covid pandemic slammed the ranks of Wall Street's independent and regional members, the Board seemed largely missing in action.With only three seats on FINRA's gerrymandered Board, the Small Firm community must move past popularity contests and seek out dedicated advocates, who will keep their promises and confront the other members of the Board if necessary. As a founder in 1998 of the NASD Dissident Movement and the successor FINRA Dissident Movement, I urge Paige Pierce and Stephen Kohn to forge an effective coalition whereby qualified Small Firm candidates are provided with the resources to win contested elections.

FINRA Annual Conference: Fireside Chat with Eileen Murray / May 17, 2022

https://www.finra.org/media-center/finra-unscripted/2022-annual-conference-eileen-murray

https://www.finra.org/media-center/finra-unscripted/2022-annual-conference-eileen-murray

A conversation from the FINRA Annual Conference between FINRA President/Chief Executive Officer Robert Cook and the FINRA Board of Governors Chair Eileen Murray

Edward Jones Sued for $15 Million Over Book of Business (BrokeAndBroker.com Blog)

https://www.brokeandbroker.com/6447/edward-jones-shotgun/

In "The Love Song of J. Alfred Prufrock," T.S. Eliot laments: "I have measured out my life with coffee spoons." In a recent federal lawsuit involving a $15 million claim against Edward Jones, a District Court laments that the Plaintiff failed to measure out his Complaint in numbered paragraphs or different counts. Alas, the Court lacks the lilting prose of the poet.