The Wall Street Legal & Regulatory Feed

Securities Industry Commentator by Bill Singer Esq

November 11, 2022

DOJ RELEASES

California Man Extradited From Australia To Face Charges For Investment Scheme (DOJ Release)

U.S. Attorney Announces Historic $3.36 Billion Cryptocurrency Seizure And Conviction In Connection With Silk Road Dark Web Fraud / In November 2021, Law Enforcement Seized Over 50,676 Bitcoin Hidden in Devices in Defendant JAMES ZHONG's Home; ZHONG Has Now Pled Guilty to Unlawfully Obtaining that Bitcoin From the Silk Road Dark Web in 2012 (DOJ Release)

SEC RELEASES

SEC Announces Additional Charges in Scheme to Trade Ahead of Pharma Tender Offer (SEC Release)

SEC Charges Pharmaceutical Co. Chief Information Officer in $8 Million Insider Trading Scheme (SEC Release)

SEC Granted Summary Judgment Against New Hampshire Issuer of Crypto Asset Securities for Registration Violations (SEC Release)

SEC Charges Creator of Global Crypto Ponzi Scheme and Three US Promoters in Connection with $295 Million Fraud / Trade Coin Club raised money from more than 100,000 investors worldwide (SEC Release)

SEC Obtains Fraud Injunction and Penny Stock Bar Against Microcap Stock Promoter (SEC Release)

SEC Denies Whistleblower Award to Two Claimants

Order Determining Whistleblower Award Claims

SEC Awards Joint $1.6 Million Whistleblower Award to Three Claimant And A $1.6 Million Whistleblower Award to Fourth Claimant

Order Determining Whistleblower Award Claims

SEC Denies Whistleblower Award to Claimant

Order Determining Whistleblower Award Claims

SEC Denies Whistleblower Award to Claimant

Order Determining Whistleblower Award Claims

SEC Denies Whistleblower Award to Claimant

Order Determining Whistleblower Award Claims

SEC Denies Whistleblower Award to Claimant

Order Determining Whistleblower Award Claims

CFTC RELEASESFINRA RELEASES

= = =

11/11/2022

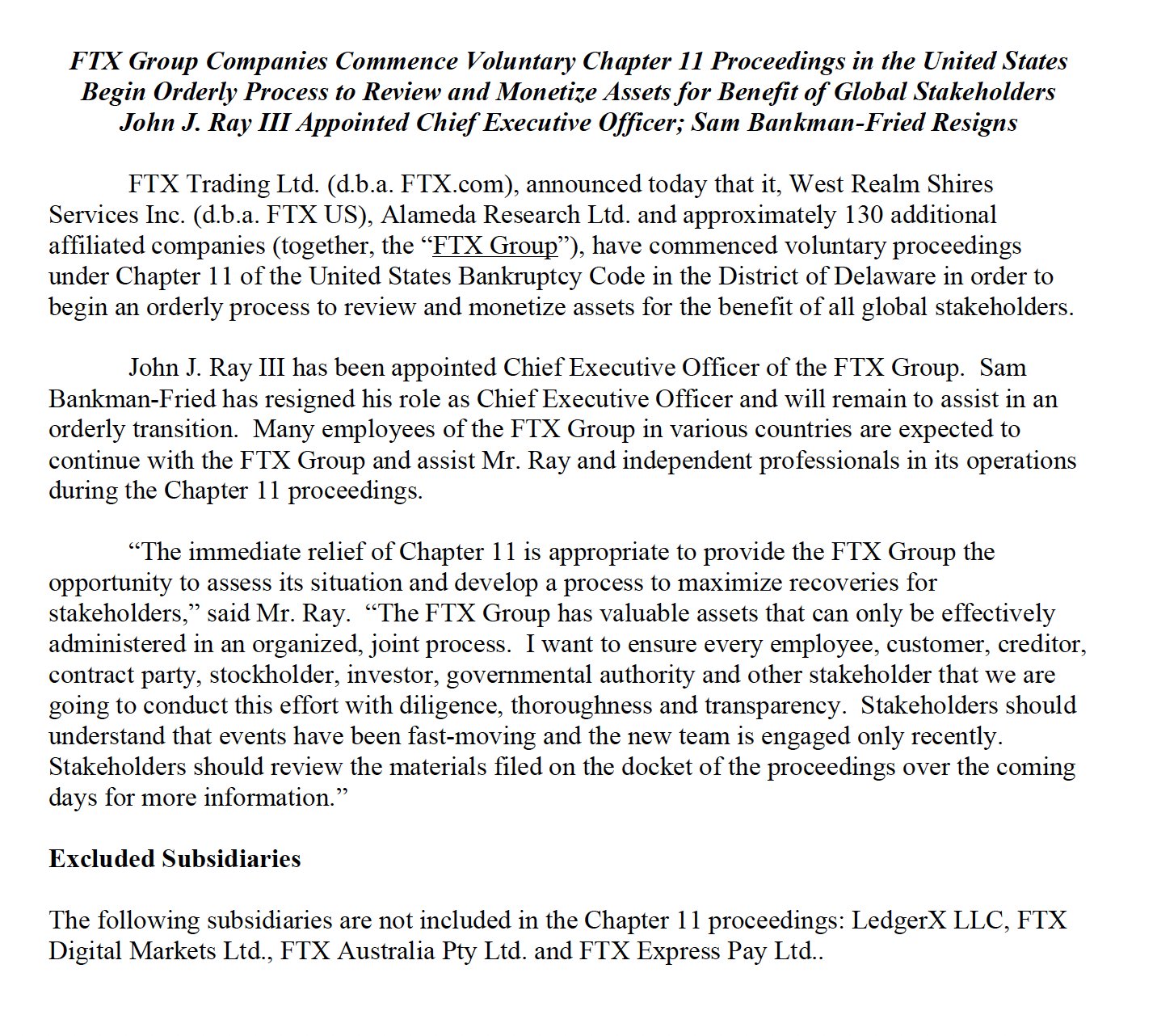

https://twitter.com/FTX_Official/status/1591071832823959552/photo/1

https://www.sec.gov/litigation/litreleases/2022/lr25576.htm

In a Complaint filed in the United States District Court for the Southern District of New York

https://www.sec.gov/litigation/complaints/2022/comp25576.pdf, the SEC charged Brian Wong with violations of the antifraud provisions of Sections 10(b) and 14(e) of the Securities Exchange Act and of Exchange Act Rules 10b-5 and 14e-3. Brian Wong consented to the entry of injunctive relief, with monetary remedies to be determined at a later date, upon a motion by the SEC. Parallel criminal charges were filed against Wong. In part the SEC Release alleges that:

https://www.sec.gov/litigation/complaints/2022/comp25576.pdf, the SEC charged Brian Wong with violations of the antifraud provisions of Sections 10(b) and 14(e) of the Securities Exchange Act and of Exchange Act Rules 10b-5 and 14e-3. Brian Wong consented to the entry of injunctive relief, with monetary remedies to be determined at a later date, upon a motion by the SEC. Parallel criminal charges were filed against Wong. In part the SEC Release alleges that:

[B]rian Wong made approximately $400,000 from illegally trading ahead of a February 2021 announcement of a tender offer by Merck & Co., Inc. to acquire Pandion Therapeutics, Inc. The SEC's complaint alleges that Brian Wong's brother, Brandon Wong, unlawfully communicated material nonpublic information about Merck's impending acquisition of Pandion to Brian Wong before the February 2021 announcement, and that Brian Wong purchased Pandion stock based on that information. As previously alleged in the SEC's July 25, 2022 complaint, Brandon Wong had been tipped about the impending acquisition by his friend Seth Markin, who had misappropriated the information from Markin's romantic partner, an attorney working on the deal.

https://www.finra.org/sites/default/files/fda_documents/2019064126802

%20Clearview%20Trading%20Advisors%2C%20Inc.%20CRD%20142873

%20Gregg%20H.%20Ettin%20CRD%201604260%20AWC%20lp.pdf

%20Clearview%20Trading%20Advisors%2C%20Inc.%20CRD%20142873

%20Gregg%20H.%20Ettin%20CRD%201604260%20AWC%20lp.pdf

For the purpose of proposing a settlement of rule violations alleged by the Financial Industry Regulatory Authority ("FINRA"), without admitting or denying the findings, prior to a regulatory hearing, and without an adjudication of any issue, Clearview Trading Advisors, Inc. and Gregg H. Ettin submitted a Letter of Acceptance, Waiver and Consent ("AWC"), which FINRA accepted.

The AWC asserts that Clearview Trading Advisors, Inc. has been a FINRA member firm since 2007 and has about six registered representatives. In accordance with the terms of the AWC, FINRA imposed upon Clearview a Censure and $10,000 fine and a six-month suspension from associating with any FINRA member in all capacities.

The AWC asserts that Gregg H. Ettin was first registered in 1986, and founded Clearview, where he served as the firm's sole owner/Chief Executive Officer, and by 2018, he held various compliance officer roles. In accordance with the terms of the AWC, FINRA imposed upon Ettin a $25,000 fine and a nine-month suspension from associating with any FINRA member in Principal-only capacities.

The AWC "Summary" asserts that:

From August 2018 to March 2019, Clearview and Ettin, the firm's AMLCO, failed to establish and implement an anti-money laundering (AML) compliance program reasonably designed to detect and cause the reporting of suspicious activity. Therefore, Clearview and Ettin violated FINRA Rules 3310(a) and 2010.During the same period, Clearview and Ettin, who was responsible for reviewing and approving customer deposits and sales of restricted securities under the firm's Written Supervisory Procedures (WSPs), failed to establish and maintain a supervisory system, including WSPs, reasonably designed to achieve compliance with Section 5 of the Securities Act of 1933. Therefore, Clearview and Ettin violated FINRA Rules 3100(a), 3110(b), and 2010.

= = =

11/10/2022

FINRA Arbitrators Slam Losing Respondents with Hearing Fees in Breach of Contract Dispute (BrokeAndBroker.com Blog)

https://www.brokeandbroker.com/6758/finra-intellivest-arbitration/

In today's featured FINRA arbitration, we got an investment banking dispute involving a breach of contract. Added into that mix, we got an inaccurate Form ADV. Frankly, there's a whole lot of nothing and a little bit of something swirling around here, but the Claimant's lawyer seems to have grabbed the arbitrators' attention and made a point. And that point rang up the proverbial cash register in Claimant's favor. In the end, the FINRA Arbitration Panel seems perturbed by Respondents' "inattentiveness" and hit them with a fee that isn't often awarded in full.

Two Defendants Charged For Nationwide Online Marketing Scheme That Fraudulently Enrolled Customers In Credit Monitoring Monthly Subscription / The Defendants Fraudulently Induced Over 2.7 Million Visits to the Defendants' Websites and Enrolled Approximately 169,000 Customers in Credit Monitoring Services Under False Pretenses, Resulting in Approximately $6.8 Million in Revenue (DOJ Release)

https://www.justice.gov/usao-sdny/pr/two-defendants-charged-nationwide-online-marketing-scheme-fraudulently-enrolled

https://www.justice.gov/usao-sdny/pr/two-defendants-charged-nationwide-online-marketing-scheme-fraudulently-enrolled

In an Indictment filed in the United States District Court for the Southern District of New York

https://www.justice.gov/usao-sdny/press-release/file/1551121/download, Michael Brown and Andrew Lloyd were each charged with one count of conspiracy to commit wire fraud and one count of wire fraud. As alleged in part in the DOJ Release:

https://www.justice.gov/usao-sdny/press-release/file/1551121/download, Michael Brown and Andrew Lloyd were each charged with one count of conspiracy to commit wire fraud and one count of wire fraud. As alleged in part in the DOJ Release:

MICHAEL BROWN owned and operated Credit Bureau Center, LLC, formerly known as MyScore LLC ("MyScore"), a Delaware limited liability company which provided credit reports and credit monitoring services via the websites eFreeScore.com, FreeCreditNation.com, and CreditUpdates.com, among other sites (collectively, the "MyScore Websites"). ANDREW LLOYD was an affiliate that worked with a co-conspirator ("CC-1"), the owner of an affiliate marketing company, to drive potential customers to the MyScore Websites. In affiliate marketing, a seller of goods or services such as MyScore uses other firms or individuals known as "affiliates" to market the seller's goods or services by attracting customers to the seller's websites. BROWN contracted with CC-1 in order to increase customer traffic to the MyScore Websites.From at least in or about 2014 through at least on or about January 10, 2017, BROWN, LLOYD, and CC-1 engaged in a nationwide online marketing scheme to post fake advertisements for rental properties across the United States on a classified advertisements website (the "Advertising Website"). The purpose of the scheme was to fraudulently induce prospective renters to enter their credit card information on the MyScore Websites and obtain a credit report under false pretenses in order to automatically enroll them in a monthly membership for credit monitoring services.The advertisements used in the scheme typically contained photos of the rental properties and showcased properties in desirable locations for below-market prices in order to attract interest. The advertisements were posted for rental properties in metropolitan areas across the United States, including, among other locations, New York City, Miami, Atlanta, Houston, Los Angeles, and San Diego. In actuality, the rental properties did not exist as advertised or were not actually available for rent through the posts on the Advertising Website. The advertisements also did not disclose the specific address of the rental properties but instead contained a contact email address inviting prospective renters to contact the property owner if they were interested in the rental property.When prospective renters inquired about the rental properties posted on the Advertising Website by responding to the advertisements, they received a form email purporting to be from the property owner requiring the prospective renter to obtain a copy of their credit report, and referring the prospective renter to one of the MyScore Websites to obtain a credit report, before scheduling a tour of the property. The form email typically described purported features of the advertised property and falsely informed the prospective renter, in substance and in part, that he or she was the second person to respond to the advertisement, that the first responder no longer needed the property, and that the property owner was ready to lease the property to the prospective renter with flexible terms and had just completed all new renovations.Once a prospective renter clicked on the hyperlink in the form email from the purported property owner to obtain a copy of their credit report, the prospective renter was directed to the "landing page" of one of the MyScore Websites. The landing page of the MyScore Websites typically featured a large banner that stated, in substance and in part, "Get Your Free Credit Score and Report" with significantly smaller text referencing an unspecified "7-day trial" and a "Monthly membership of $29.94 automatically charged after trial." In order to get the credit report, prospective renters were required to enter identifying information and credit card information through a series of webpages. Once the prospective renter entered credit card information, the prospective renter was charged $1.00 and was automatically enrolled in a monthly membership for credit monitoring services with recurring charges of typically $29.94 per month until the membership was cancelled.When prospective renters responded to the purported property owner asking to schedule a tour of the advertised property now that they had a copy of their credit report, there was typically no response, as the property was not actually available for rent as advertised and the scheme had succeeded in fraudulently generating a monthly membership subscription for MyScore. Many prospective renters who obtained a credit report from the MyScore Websites as a result of the scheme did not realize that they had been automatically enrolled in MyScore's membership until they discovered the monthly charges on their credit card statements. Some prospective renters also had difficulties canceling the membership when they contacted MyScore's customer service department.BROWN, LLOYD, and CC-1 continued to execute the scheme through at least on or about January 10, 2017, despite numerous complaints during the course of the scheme from customers and consumer organizations about the fraudulent nature of the rental advertisements on the Advertising Website, the automatic enrollment of customers in MyScore's monthly membership with recurring charges without their knowledge, and the difficulties in cancelling the monthly membership.In total, the scheme caused over approximately 2.7 million unique visits to the MyScore Websites and generated approximately $6.8 million in revenue from approximately 169,000 customers who were automatically enrolled in MyScore's monthly membership for credit monitoring services through the scheme.

Chief Information Officer of Publicly Traded Pharmaceutical Company Charged for Insider Trading Scheme (DOJ Release)

https://www.justice.gov/opa/pr/chief-information-officer-publicly-traded-pharmaceutical-company-charged-insider-trading

-and

SEC Charges Pharmaceutical Co. Chief Information Officer in $8 Million Insider Trading Scheme (SEC Release)

https://www.sec.gov/news/press-release/2022-204

As alleged in part in the DOJ Release:

[R]amkumar Rayapureddy, 54, of Upper Saint Clair, conspired with his former colleague, Dayakar Mallu, to fraudulently trade in Mylan securities based on material nonpublic inside information Rayapureddy obtained through his position at Mylan in advance of market-moving corporate announcements for their own financial gain. At the time of the alleged scheme, Rayapureddy was Mylan's chief information officer.From 2017 through 2019, Rayapureddy allegedly tipped Mallu on multiple occasions with material nonpublic inside information about Mylan concerning, among other things, FDA drug approvals, financial earnings, and a merger with a division of Pfizer, Inc. Mallu allegedly used the inside information to execute trades in the company's securities and in return Rayapureddy or his designee received cash payments.Rayapureddy is charged with one count of conspiracy to commit securities fraud and three counts of securities fraud. If convicted, he faces a maximum penalty of 20 years in prison on each of the securities fraud charges and five years in prison on the conspiracy charge. A federal district court judge will determine any sentence after considering the U.S. Sentencing Guidelines and other statutory factors.In September 2021, Mallu pleaded guilty to conspiracy to commit securities fraud and aiding in the preparation of a false tax return and is awaiting sentencing.

In a Complaint filed in the United States District Court for the Western District of Pennsylvania, the SEC charged Viatris Inc.'s (f/k/a "Myalan N.V.") Chief Information Officer Ramkumar Rayapureddy, Chief Information Officer of pharmaceutical company Viatris Inc., which was formerly known as Mylan N.V. with with violating Section 10(b) of the Securities Exchange Act and Rule 10b-5 thereunder. As alleged in part in the SEC Release:

[F]rom at least September 2017 through July 2019, Rayapureddy, a resident of Pennsylvania, tipped his friend and former colleague, Dayakar Mallu, material nonpublic information about Mylan's unannounced drug approval by the U.S. Food & Drug Administration, financial results, and an impending merger with a division of Pfizer Inc. The complaint further alleges that Mallu generated gains totaling nearly $8 million and avoided losses by trading Mylan securities based upon Rayapureddy's tips and shared a portion of his profits with Rayapureddy through cash payments in India. The SEC previously charged Mallu in connection with this investigation.

https://www.finra.org/sites/default/files/fda_documents/2021072841801

%20Ellen%20Gayle%20Reynard%20CRD%206148906%20AWC%20va.pdf

%20Ellen%20Gayle%20Reynard%20CRD%206148906%20AWC%20va.pdf

For the purpose of proposing a settlement of rule violations alleged by the Financial Industry Regulatory Authority ("FINRA"), without admitting or denying the findings, prior to a regulatory hearing, and without an adjudication of any issue, Ellen Gayle Reynard submitted a Letter of Acceptance, Waiver and Consent ("AWC"), which FINRA accepted. The AWC asserts that Ellen Gayle Reynard entered the industry in 2012, and from April 2013 to October 13, 2021, she was registered with Raymond James Financial Services, Inc. In accordance with the terms of the AWC, FINRA imposed upon Reynard a $5,000 fine and a five-month suspension from associating with any FINRA member in all capacities. The AWC asserts in part that:

From December 2018 to May 2021, Reynard falsified 171 forms associated with money movements from seven customer accounts. Reynard directed the customers to sign blank or incomplete forms, but neither Reynard nor the customers completed or submitted the forms at the time Reynard obtained their signatures. Instead, Reynard maintained the blank, signed forms, which she later photocopied, completed and submitted to Raymond James at the customers' requests. 168 of the falsified forms authorized approximately $23,000 in money movements from five customer accounts. The remaining three falsified forms authorized the establishment of customer profiles facilitating money movements from two customer accounts: two forms established Automated Clearing House (ACH) profiles for a customer, and one form was a standing letter of authorization for another customer.By falsifying forms associated with money movements from customer accounts, Reynard violated FINRA Rule 2010. In addition, Reynard violated FINRA Rules 4511 and 2010 by causing Raymond James to maintain inaccurate books and records.

FINRA Fines and Suspends Rep for Borrowing and Repaying About $7.3 Million from Customers Without Notice to Firm

In the Matter of Theodore M. Serure, Respondent (FINRA AWC 2019063945301)

https://www.finra.org/sites/default/files/fda_documents/2019063945301

%20Theodore%20M.%20Serure%20CRD%20419023%20AWC%20gg.pdf

%20Theodore%20M.%20Serure%20CRD%20419023%20AWC%20gg.pdf

For the purpose of proposing a settlement of rule violations alleged by the Financial Industry Regulatory Authority ("FINRA"), without admitting or denying the findings, prior to a regulatory hearing, and without an adjudication of any issue, Theodore M. Serure submitted a Letter of Acceptance, Waiver and Consent ("AWC"), which FINRA accepted. The AWC asserts that Theodore M. Serure entered the industry in 1968, and from October 1979 through November September 2019, he was registered with J.P. Morgan Securities, LLC. and, thereafter, with Jefferies LLC. In accordance with the terms of the AWC, FINRA imposed upon Serure a $20,000 fine and a four-month suspension from associating with any FINRA member in all capacities. The AWC asserts in part that:

Between 2014 and 2020, Serure borrowed a total of approximately $7.3 million from sixteen of his customers, without providing notice to or receiving prior written approval from JPMS or Jefferies LLC. Serure was never indebted to his customers at any time for more than $2 million since he used some of the loan proceeds to pay off earlier customer loans. Serure repaid all of the customer loans, and none of the customers complained. All of the customers from whom Serure borrowed money were wealthy and financially sophisticated. For example, one is a billionaire, another is a Nobel Prize winner, and a third is the former CEO of a major financial institution. Serure had been close friends with each customer for decades, some since childhood. Given his personal relationship with each of the customers, the loans fell within FINRA Rule 3240(a)(2)(D), but Serure failed to notify his firms of or obtain their approval for the loans.By virtue of the foregoing, Serure violated FINRA Rules 3240 and 2010.

Bill Singer's Comment: Ummm . . . uhhhh . . .. hmmmm . . he repaid all the loans, and, the loans would have been okay per the "personal relationship" exception, but, sure, he needed to notify the firm, and, okay, he didn't, but, FINRA only imposed a four-month suspension and $20,0000 fine . . . so . . . I dunno . . . seems a tad ticky-tacky but FINRA sort of pulled its punches, and, he was wrong, but no one was harmed, and, oh well, not everything in life or regulation is nice and neat, right?

In the Matter of Christopher Eriksson, Respondent (FINRA AWC 2020068025901)

https://www.finra.org/sites/default/files/fda_documents/2020068025901

%20Christopher%20Eriksson%20CRD%202487298%20AWC%20gg.pdf

%20Christopher%20Eriksson%20CRD%202487298%20AWC%20gg.pdf

For the purpose of proposing a settlement of rule violations alleged by the Financial Industry Regulatory Authority ("FINRA"), without admitting or denying the findings, prior to a regulatory hearing, and without an adjudication of any issue, Christopher Eriksson submitted a Letter of Acceptance, Waiver and Consent ("AWC"), which FINRA accepted. The AWC asserts that Christopher Eriksson entered the industry in 1994 and by January 2005, he was registered with Merrill Lynch, Pierce, Fenner & Smith Incorporated. In accordance with the terms of the AWC, FINRA imposed upon Eriksson a $10,000 fine and a six-month suspension from associating with any FINRA member in all capacities. The AWC asserts in part that:

In April 2018, while registered through Merrill Lynch, Eriksson borrowed $350,000 from Customer A, at a fixed interest rate, as documented by a promissory note drafted by one of the co-trustees of Customer A. Eriksson has paid off in full the principal and interest on the loan.At the time Eriksson entered into the loan agreement, Merrill Lynch's written supervisory procedures prohibited its registered representatives from borrowing money from a customer, unless the customer was a family member, and the firm approved the loan. Customer A was not Eriksson's family member, and Eriksson did not seek or obtain prior approval of the loan from Merrill Lynch.

Therefore, Respondent violated FINRA Rules 3240 and 2010.. . .In February 2018, Eriksson formed USAR LLC (USAR), in which two of his friends later obtained an ownership interest. In October 2018, USAR purchased a parcel of land in Texas from Customer A to develop an auto recycling business. Eriksson did not disclose USAR to Merrill Lynch, nor did he receive approval for this outside business activity.In September 2003, Eriksson organized Eriksson Family Properties, LLC (EFP), of which he is the sole owner. EFP acquired two commercial properties in St. Paul, Minnesota. EFP received rental payments for one of the properties from 2010 to 2015, and rented the other property in 2018 on a monthly basis. Eriksson did not disclose EFP to Merrill Lynch until April 2020, at which time the firm granted approval.In September 2015, Eriksson purchased an ownership interest in three automobile salvage companies and two related real estate holding companies. Eriksson never disclosed his ownership of these entities to Merrill Lynch, nor did he receive approval for this outside business activity.Additionally, in 2017, 2018, and 2019, Eriksson submitted questionnaire responses to Merrill Lynch which failed to disclose all his outside business activities.Therefore, Respondent violated NASD Rules 3030 and 2110, and FINRA Rules 3270 and 2010.

= = =

11/9/2022

Wade Roberts, Plaintiff/Appellant, v. Wells Fargo Clearing Services, LLC, Defendant/Appellee (Opinion, United States Court of Appeals for the Eleventh Circuit, 22-11049 / November 9, 2022)

https://brokeandbroker.com/PDF/Roberts11CirOp221109.pdf

In pertinent parts, the 11Cir Opinion alleges that:

Wade Roberts appeals an order compelling him to arbitrate his complaint against his former employer, Wells Fargo Clearing Services, LLC, for collecting the balance he owed on outstanding loans. The district court ruled that Roberts had agreed to arbitrate with Wells Services in his offer of employment letter and in promissory notes he executed to obtain advances on his compensation. We affirm.

at Page 2 of the 11Cir Opinion

. . .

Between August 2016 and July 2021, Roberts obtained five loans from Wells Services for which he executed promissory notes. The loans operated as advances against future bonuses. The dates and amounts of the loans were as follows: August 19, 2016, for $788,128; September 22, 2017, for $274,132; November 16, 2017, for $171,332; November 27, 2018, for $171,332; and November 30, 2019, for $171,332.

at Page 4 of the 11Cir Opinion

. . .

In July 2021, Roberts resigned from Wells Services. Its collections department notified Roberts that he had an outstanding balance of $809,965.26 on his loans, which he refused to pay. Wells Services garnished Roberts's bank accounts to satisfy the debt.Roberts filed a complaint in a Georgia court against Wells Services for conversion and improper solicitation of money. Roberts denied receiving a loan or "funds . . . other than employee compensation from" Wells Services. Wells Services removed Roberts's action to the district court, see 18 U.S.C. § 1332, and then moved to compel arbitration based on Rule 13200 of the Code of Arbitration Procedure for Industry Disputes and to dismiss the complaint.The district court granted the motion to compel arbitration and dismissed Roberts's complaint without prejudice. The district court ruled that the arbitration clauses in Roberts's employment letter and five promissory notes were enforceable under Georgia law and applied to his claims against Wells Services. The district court rejected Roberts's arguments that the notes were unenforceable.

at Page 6 of the 11Cir Opinion

. . .

The district court did not err by ordering Roberts to arbitrate his claims against Wells Services under Rule 13200. Roberts signed multiple documents, including a form U-4 and five promissory notes in which he agreed to arbitrate controversies connected to his employment with and the advances he received from Wells Services. See Kidd v. Equitable Life Assur. Soc. of U.S., 32 F.3d 516, 520 (11th Cir. 1994) ("If the NASD did not mandate arbitration of employer-employee disputes, there would be no reason to require Appellees to sign U-4 forms promising to arbitrate such disputes."). Roberts does not dispute the validity of those documents or his agreements to arbitrate. He concedes that he is an associated person and that Wells Services is a member. And the allegations that form the basis of the dispute "arise out of the business activities" between Roberts and Wells Services. See FINRA Rule 13200. Roberts is bound by his agreements to arbitrate

at Page 10 of the 11Cir Opinion

TD Ameritrade Loses FINRA Customer Arbitration Citing Inaccurate Statements and Forced Liquidation (BrokeAndBroker.com Blog)

https://www.brokeandbroker.com/6757/td-ameritrade-arbitration/

A lowly pro se Claimant took on one of FINRA's Big Boys in an arbitration seeking less than $9,000 in alleged damages. Why didn't TD Ameritrade just settle the damn lawsuit and be done with it? I don't know and the FINRA Award doesn't explain. Another thing left unanswered is why the winning customer got about half of what he asked for, why he was allegedly forced to liquidate his account, and why FINRA imposed fees upon this victorious small fry.

https://www.justice.gov/usao-wdtx/pr/san-antonio-couple-sentenced-restaurant-investment-fraud-scheme

In the United States District Court for the Western District of Texas, Juan Enrique Kramer, 46, pled guilty to one count of conspiracy to commit wire fraud and one count of failure to file an individual tax return; and Kramer's wife, Adriana Pastor, 47, pled guilty to one count of aiding or assisting in filing a false tax return. Kramer was sentenced to three years in prison plus three years of supervised release, ordered to forfeit 59,589 in proceeds, and ordered to pay restitution of $1,171,497 to victims and $727,936 to the IRS. Pastor was sentenced to 18 months in prison plus three years of supervised release, and is also liable for the $727,936 to the IRS. As alleged in part in the DOJ Release:

[K]ramer and other co-conspirators promoted a "turn-key" business venture to Mexican nationals, consisting of a chain of Mexican food restaurants throughout the United States and Mexico known as "Las Quesadillas." Kramer charged buyers a set fee ranging from $105,000 to $250,000 and promised to perform all tasks necessary for establishing a fully functional restaurant, including finding and renting a suitable location; obtaining all permits; providing assistance in obtaining visas for buyers; completing construction; training employees; and handling all legal fees and incorporation issues.The defendants took funds from buyers but failed to provide the promised services. Instead, they used the funds for personal gain or to provide partial payments to previous customers who were demanding their money back. In addition to partial refunds, Kramer would also offer stakes in other businesses as an alternative to repayment. If buyers refused, Kramer would threaten to sue them for breach of contract. The defendants perpetrated their scheme on at least eight different victims resulting in a total loss of more than $1 million.. . .Kramer and Pastor did not declare any of the investor income to the IRS. In 2016, Pastor signed a tax return which falsely stated a net income loss. In 2017 and 2018, the couple did not file any tax returns whatsoever, despite still running restaurants and taking in investor money.

= = =

11/8/2022

https://www.supremecourt.gov/qp/21-01239qp.pdf

QUESTION PRESENTED:Whether a federal district court has jurisdiction to hear a suit in which the respondent in an ongoing Securities and Exchange Commission administrative proceeding seeks to enjoin that proceeding, based on an alleged constitutional defect in the statutory provisions that govern the removal of the administrative law judge who will conduct the proceeding.LOWER COURT CASE NUMBER: 19-10396

https://www.supremecourt.gov/qp/21-00086qp.pdf

QUESTION PRESENTED:

After petitioner acquired an essentially insolvent competitor, it found itself subjected to the review of the Federal Trade Commission (FTC), rather than the Department of Justice (DOJ). While the DOJ route promises early access to judicial review, the FTC track is an altogether different matter. Petitioner faced a series of unreasonable demands from the FTC, and the prospect of "litigating" before administrative law judges insulated by unconstitutional double-for-cause removal restrictions and subject to review by an unaccountable Commission. Rather than resign itself to the ongoing unconstitutional injuries inflicted by the FTC's process, petitioner filed suit in district court seeking to enjoin the unconstitutional FTC proceedings. That lawsuit focused on constitutional issues collateral to the underlying antitrust issues, but the district court nonetheless dismissed it for want of jurisdiction based on implications drawn from a statutory grant of jurisdiction to review the FTC's cease-and-desist orders. A divided Ninth Circuit affirmed, with the majority acknowledging that dismissal "makes little sense," and the dissent contending that dismissal contradicted this Court's precedents.The questions presented are:1. Whether Congress impliedly stripped federal district courts of jurisdiction overconstitutional challenges to the Federal Trade Commission's structure, procedures, and existence by granting the courts of appeals jurisdiction to "affirm, enforce, modify, or set aside" the Commission's cease-and-desist orders.2. Whether, on the merits, the structure of the Federal Trade Commission, including the dual-layer for-cause removal protections afforded its administrative law judges, is consistent with the Constitution.

LOWER COURT CASE NUMBER: 20-15662

Michigan Man Sentenced to 3 1/2Years in Prison for Role in 'SIM Swapping' that Led to Account Takeovers and $122,000 in Losses (DOJ Release)

https://www.justice.gov/usao-cdca/pr/michigan-man-sentenced-3-years-prison-role-sim-swapping-led-account-takeovers-and

In the United States District Court for the Central District of California, Anthony Joseph Carlson, 25, pled guilty to two counts of conspiracy to commit wire fraud and two counts of unauthorized access to a protected computer to obtain information; and he was sentenced to 42 months in prison in connection with a Subscriber Identification Module ("SIM") swapping.

Carlson participated in two separate conspiracies to use SIM swapping to gain unauthorized access to the email, financial and social media accounts of the victims to steal cryptocurrency. One scheme that did not result in any actual losses involved the takeover of a Coinbase account in order to steal $10,000 in cryptocurrency, and a second involved the takeover of a Facebook account that allowed Carlson and a co-conspirator to obtain cryptocurrency from two friends of the person whose account had been compromised.As a result of a separate phishing scheme - in which Carlson sent emails purporting to be from a legitimate source to induce victims to reveal information, including personal identifying information and passwords - he was able to gain control of valuable Instagram accounts with large numbers of followers. Carlson told the victims who owned the Instagram accounts that he wanted to purchase advertising on their accounts, but he needed to first determine how valuable their accounts were for marketing purposes. Carlson convinced the victims to download his purported analytics software, which had a spoofed website name almost identical to a commonly used Instagram analytics software, and they were tricked into providing their Instagram usernames and passwords, which Carlson used to take over their Instagram accounts to monetize for his personal gain.Carlson also obtained stolen Instagram accounts from others and then re-sold them to other victims for thousands of dollars. In another scheme, Carlson collected money for advertising on Instagram accounts he did not actually control.

Fraudster Pleads Guilty to Participating in an $800,000 Elder Fraud Scam / Anderson Posed as a Bail Bondsman and Courier to Retrieve Fraud Proceeds Directly from Victims (DOJ Release)

https://www.justice.gov/usao-md/pr/fraudster-pleads-guilty-participating-800000-elder-fraud-scam

In the United States District Court for the District of Maryland, Michael Odell Anderson, 64, nd Dun Lorring pled guilty to conspiracy to commit wire fraud n relation to his participation in an elder fraud scam. Anderson will pay up to $578,170 in restitution and forfeit assets including $70,327 in seized cash. As alleged in part in the DOJ Release:

[F]rom April 2020 to December 2020, Anderson conspired with others to persuade elderly victims to give them thousands of dollars under false pretenses. Specifically, members of the conspiracy called elderly victims posing as a police officer, lawyer, or relative and convinced victims to send money for the purported legal expenses of a loved one, generally a grandchild, who had been incarcerated in connection with a car accident or traffic stop involving a crime.If victims provided cash as directed by conspirators, conspirators fabricated additional reasons for them to send more money, claiming the additional funds were necessary for their grandchild's legal expenses, bail costs, fines, or to pay damages. Conspiracy members continued to call victims and demand additional funds, regularly obtaining tens of thousands of dollars from the retirement savings of victims. Additionally, conspirators falsely told the victims that the money they sent would be returned to them at a later date. To conceal the crime, the co-conspirators often told the victims that there had been a "gag order" placed on the case requiring secrecy and that the victim could not share the information with others.Anderson admitted that he and other conspirators posed as bail bondsmen or couriers and received cash directly from the victims, taking approximately seven percent of the proceeds as their payment and distributing the remaining fraud proceeds to other conspirators. To conceal their identities, Anderson and the other conspirators used fake names and would not park directly in front of the victims' homes when retrieving cash from the victims. When Anderson was recruited into the conspiracy in April 2020, he traveled to the Maryland area to perpetrate the scheme, collecting money from victims in Maryland, Virginia, Delaware, and other states. As part of the conspiracy, Anderson recruited additional participants to join the conspiracy and assist in retrieving cash from the victims. Anderson directed the recruited conspirators to pay him a percentage of their earnings from the fraud scheme.For example, Anderson, posing as a bail bondsman, traveled to Sykesville, Maryland on December 4, 2020, and collected $29,000 in cash from Victim 3, who had received a call from a co-conspirator telling her that her nephew had been arrested and needed money for his bail. The next day, Victim 3 received another call and was told that she needed to pay an additional $10,000 in cash for bail money. Anderson again traveled to Victim 3's home to collect the cash and was arrested while attempting to retrieve the money.As a result of the scheme, Anderson and the other conspirators caused at least 49 victims to pay at least $842,670 through materially false pretenses, representation, and promises. Of that amount, approximately $578,170 was not returned to the victims

Colorado man who defrauded Montana family of nearly $400,000 in African gold investment scheme sentenced to 27 months in prison (DOJ Release)

https://www.justice.gov/usao-mt/pr/colorado-man-who-defrauded-montana-family-nearly-400000-african-gold-investment-scheme

In the United States District Court for the District of Montana, Geoffrey Wescott James, 59, pled guilty to wire fraud; and he was sentenced to 27 months in prison plus three years of supervised release, and fined $5,000. As alleged in part in the DOJ Release [Ed: DOJ Release oddly refers to Defendant as both Wescott and James]:

[F]rom May 2019 until September 2020, Wescott falsely claimed he would receive payments from victims, which he would then transfer to Africa on behalf of victims for investments in overseas gold. The investment appeared enticing to victims because, among other reasons, it offered high rates of return in a short period of time. Because victims had difficulties in sending money overseas and to Africa, they were introduced to James. Instead of transferring the money overseas and to Africa for the intended purpose, James spent the money on items for himself and for other unauthorized purposes. When victims questioned where their money was located and demanded that their money be returned, James repeatedly claimed the money would be repaid soon, none of which was true. Wescott defrauded a family in Hill County of $391,280 in the scheme.

https://www.justice.gov/usao-wdnc/pr/california-man-extradited-australia-face-charges-investment-scheme

In the United States District court for the Western District of North Carolina, Gustavo Guzman was charged with wire fraud, securities fraud and transactional money laundering charges. As alleged in part in the DOJ Release;

[F]rom April 2010 to August 2015, Guzman, through various entities he controlled, including G2 Asset Management and East Egg Private Equity, executed a scheme to defraud approximately 10 investors of at least $2 million, by falsely representing that he would use the investors' money to trade in options and other similar investments. Instead of investing the funds as promised, Guzman allegedly stole a substantial portion of the investors' money and used it to fund his personal lifestyle, including to make large credit card payments and cash withdrawals, and to pay for personal expenditures. As alleged in the indictment, Guzman suffered massive trading losses with the money that he did invest and used some of the victim's money to make Ponzi-style payments to investors. To conceal the trading losses and the fraudulent scheme, and to prevent his victims from redeeming their investments and complaining to authorities, the indictment alleges that Guzman lied to his victims about the status of their investments, and provided them with fake documents, including sham IRS forms and fraudulent account statements.

SEC Granted Summary Judgment Against New Hampshire Issuer of Crypto Asset Securities for Registration Violations (SEC Release)

https://www.sec.gov/litigation/litreleases/2022/lr25573.htm

https://www.sec.gov/litigation/litreleases/2022/lr25573.htm

In the United States District Court for the District of New Hampshire, the SEC was granted Summary Judgment on its Motion against LBRY, Inc. and the Court held that LBRY offered and sold LBC crypto asset securities in violation of the registration provisions of the federal securities laws, and that LBRY did not have a defense that it lacked fair notice of the application of those laws to its offer and sale. As alleged in part in the SEC Release:

The SEC's complaint charges LBRY with conducting an unregistered offering and sale of crypto asset securities. The SEC seeks permanent injunctive relief, disgorgement plus prejudgment interest, and civil penalties. The SEC's complaint alleged that, from at least July 2016 to February 2021, LBRY, which provides a video sharing application, sold crypto asset securities called "LBRY Credits" to numerous investors, including investors based in the US. The complaint alleges that this was an offering and sale of securities under the federal securities laws, and that LBRY did not file a registration statement for the offering. The complaint further alleges that by failing to file a registration statement, LBRY denied prospective investors the information required for such an offering to the public. The SEC's filings with the court alleged that LBRY received approximately $12.2 million in proceeds in U.S. dollars and crypto assets from its sales of LBC. The Court found that LBRY violated the charged provisions and reserved the determination of relief for a later date.

= = =

11/7/2022

The Gensler SEC's Rulemaking Reach Exceeds Its Grasp (BrokeAndBroker.com Blog)

https://www.brokeandbroker.com/6747/sec-gensler-rulemaking/

Among Henry David Thoreau's more memorable quotes is this one: "Any fool can make a rule, and any fool will mind it." Which brings me to the issue of Securities and Exchange Commission ("SEC") Chair Gary Gensler's ambitious rule-proposal agenda. Many Wall Street stakeholders fear that the large number of proposals has become excessive. There is reach. There is grasp. Our reach exceeds our grasp. I wonder whether SEC Chair Gensler has stretched out his fingers and then retracted them in order to confirm that truth.

U.S. Attorney Announces Historic $3.36 Billion Cryptocurrency Seizure And Conviction In Connection With Silk Road Dark Web Fraud / In November 2021, Law Enforcement Seized Over 50,676 Bitcoin Hidden in Devices in Defendant JAMES ZHONG's Home; ZHONG Has Now Pled Guilty to Unlawfully Obtaining that Bitcoin From the Silk Road Dark Web in 2012 (DOJ Release)

https://www.justice.gov/usao-sdny/pr/us-attorney-announces-historic-336-billion-cryptocurrency-seizure-and-conviction

In the United States District Court for the Southern District of New York, James Zhong pled guilty to one count of wire fraud. As alleged in part in the DOJ Release:

ZHONG's Scheme to Defraud

Silk Road was an online "darknet" black market. In operation from approximately 2011 until 2013, Silk Road was used by numerous drug dealers and other unlawful vendors to distribute massive quantities of illegal drugs and other illicit goods and services to many buyers and to launder all funds passing through it. In 2015, following a groundbreaking prosecution by this Office, Silk Road's founder Ross Ulbricht was convicted by a unanimous jury and sentenced to life in prison.

In September 2012, ZHONG executed a scheme to defraud Silk Road of its money and property by (a) creating a string of approximately nine Silk Road accounts (the "Fraud Accounts") in a manner designed to conceal his identity; (b) triggering over 140 transactions in rapid succession in order to trick Silk Road's withdrawal-processing system into releasing approximately 50,000 Bitcoin from its Bitcoin-based payment system into ZHONG's accounts; and (c) transferring this Bitcoin into a variety of separate addresses also under ZHONG's control, all in a manner designed to prevent detection, conceal his identity and ownership, and obfuscate the Bitcoin's source.

While executing the September 2012 fraud, ZHONG did not list any item or service for sale on Silk Road, nor did he buy any item or service on Silk Road. ZHONG registered the accounts by providing the bare minimum of information required by Silk Road to create the account; the Fraud Accounts were merely a conduit for ZHONG to defraud Silk Road of Bitcoin.

ZHONG funded the Fraud Accounts with an initial deposit of between 200 and 2,000 Bitcoin. After the initial deposit, ZHONG then quickly executed a series of withdrawals. Through his scheme to defraud, ZHONG was able to withdraw many times more Bitcoin out of Silk Road than he had deposited in the first instance. As an example, on September 19, 2012, ZHONG deposited 500 Bitcoin into a Silk Road wallet. Less than five seconds after making the initial deposit, ZHONG executed five withdrawals of 500 Bitcoin in rapid succession - i.e., within the same second - resulting in a net gain of 2,000 Bitcoin. As another example, a different Fraud Account made a single deposit and over 50 Bitcoin withdrawals before the account ceased its activity. ZHONG moved this Bitcoin out of Silk Road and, in a matter of days, consolidated them into two high-value amounts.

Nearly five years after ZHONG's fraud, in August 2017, solely by virtue of ZHONG's possession of the 50,000 Bitcoin that he unlawfully obtained from Silk Road, ZHONG received a matching amount of a related cryptocurrency - 50,000 Bitcoin Cash ("BCH Crime Proceeds") - on top of the 50,000 Bitcoin. In August 2017, in a hard fork coin split, Bitcoin split into two cryptocurrencies, traditional Bitcoin and Bitcoin Cash ("BCH"). When this split occurred, any Bitcoin address that had a Bitcoin balance (as ZHONG's addresses did) now had the exact same balance on both the Bitcoin blockchain and on the Bitcoin Cash blockchain. As of August 2017, ZHONG thus possessed 50,000 BCH in addition to the 50,000 Bitcoin that ZHONG unlawfully obtained from Silk Road. ZHONG thereafter exchanged through an overseas cryptocurrency exchange all of the BCH Crime Proceeds for additional Bitcoin, amounting to approximately 3,500 Bitcoin of additional crime proceeds. Collectively, by the last quarter of 2017, ZHONG thus possessed approximately 53,500 Bitcoin of total crime proceeds (the "Crime Proceeds").

The Government's Seizure of Forfeitable Property

On November 9, 2021, pursuant to a judicially authorized premises search warrant (the "Search"), IRS-CI agents recovered approximately 50,491.06251844 Bitcoin of the Crime Proceeds from ZHONG's Gainesville, Georgia, house. Specifically, law enforcement located 50,491.06251844 Bitcoin of the approximately 53,500 Bitcoin Crime Proceeds (a) in an underground floor safe; and (b) on a single-board computer that was submerged under blankets in a popcorn tin stored in a bathroom closet. In addition, law enforcement recovered $661,900 in cash, 25 Casascius coins (physical bitcoin) with an approximate value of 174 Bitcoin, 11.1160005300044 additional Bitcoin, and four one-ounce silver-colored bars, three one-ounce gold-colored bars, four 10-ounce silver-colored bars, and one gold-colored coin.

Beginning in or around March 2022, ZHONG began voluntarily surrendering to the Government additional Bitcoin that ZHONG had access to and had not dissipated. In total, ZHONG voluntarily surrendered 1,004.14621836 additional Bitcoin.

Forfeiture Actions

In connection with ZHONG's guilty plea, on November 4, 2022, Judge Gardephe entered a Consent Preliminary Order of Forfeiture as to Specific Property and Substitute Assets/Money Judgment forfeiting ZHONG's interest in the following property:

- ZHONG's 80% interest in RE&D Investments, LLC, a Memphis-based company with substantial real estate holdings;

- $661,900 in United States currency seized from ZHONG's home on November 9, 2021;

- Metal items, consisting of four one-ounce silver-colored bars, three one-ounce gold-colored bars, four 10-ounce silver-colored bars, and one gold-colored coin, all seized from ZHONG's home on November 9, 2021;

- 11.1160005300044 Bitcoin seized from ZHONG's home on November 9, 2021;

- 25 Casascius coins (physical Bitcoin) with an approximate value of 174 Bitcoin, collectively, seized from ZHONG's home on November 9, 2021;

- 23.7112850 Bitcoin provided by ZHONG on April 27, 2022;

- 115.02532155 Bitcoin provided by ZHONG on April 28, 2022; and

- 4.57427222 Bitcoin provided by ZHONG on June 8, 2022.

Today, in United States v. Ross Ulbricht, S1 14 Cr. 68 (LGS), the Government filed a motion for entry of an Amended Preliminary Order of Forfeiture, seeking to forfeit approximately 51,351.89785803 Bitcoin traceable to Silk Road, valued at approximately $3,388,817,011.90 at the time of seizure, as follows:

- 50,491.06251844 Bitcoin seized from ZHONG's home on November 9, 2021;

- 825.38833159 Bitcoin provided by ZHONG on March 25, 2022; and

- 35.4470080 Bitcoin provided by ZHONG on May 25, 2022.

SEC Charges Creator of Global Crypto Ponzi Scheme and Three US Promoters in Connection with $295 Million Fraud / Trade Coin Club raised money from more than 100,000 investors worldwide (SEC Release)

https://www.sec.gov/news/press-release/2022-201

In the United States District Court for the Western District of Washington, the SEC filed a Complaint alleging that

- Douver Torres Braga violated the antifraud and securities registration provisions;

- Joff Paradise violated the antifraud, securities registration, and broker-dealer registration provisions, and

- Keleionalani Akana Taylor violated the securities and broker-dealer registration provisions of the federal securities laws.

The Braga/Paradise/Taylor Complaint: https://www.sec.gov/litigation/complaints/2022/comp-pr2002-201-braga.pdf

https://www.sec.gov/litigation/complaints/2022/comp-pr2002-201-tetreault.pdf alleging that he violated the securities and broker-dealer registration provisions of the federal securities laws. Without admitting or denying the allegations in the SEC Complaint, Tetreault agreed to settle charges. As alleged in part in the SEC Release:

[B]raga created and controlled Trade Coin Club, a multi-level marketing program that operated from 2016 through 2018 and promised profits from the trading activities of a purported crypto asset trading bot. The SEC alleges that Braga and Paradise lured investors with false representations that the bot made "millions of microtransactions" every second, and that investors would receive minimum returns of 0.35 percent daily. However, instead of deploying investor funds for the purported trading bot, Braga allegedly siphoned off investor funds for his own benefit and to pay a network of worldwide Trade Coin Club promoters, including Paradise, Taylor, and Tetreault.The SEC further alleges that Trade Coin Club operated as a Ponzi scheme and that investor withdrawals came entirely from deposits made by investors, not from any crypto asset trading activity by a bot or otherwise. The complaint further alleges that Braga personally received at least 8,396 bitcoin of the amounts invested (worth $55 million at the time), Paradise received 238 bitcoin (worth more than $1.4 million at the time), Taylor received 735 bitcoin (worth more than $2.6 million at the time), and Tetreault received 158 bitcoin (worth more than $625,000 at the time).

https://www.sec.gov/litigation/litreleases/2022/lr25572.htm

In the United States District Court for the Western District of Washington, the SEC filed a Complaint alleging that David Ferraro violated Section 17(a) of the Securities Act and Section 10(b) of the Securities Exchange Act and Rule 10b-5 thereunder. Without admitting or denying the allegations in the Complaint, Ferraro consented to a bifurcated settlement, agreeing to be permanently enjoined from violations of the charged provisions and from participating in any offering of a penny stock.

The Court entered a consent judgment against Ferraro for his role in an alleged microcap stock promotion scheme that generated approximately $792,000 in trading profits for Ferraro and Justin Costello. In part, the SEC Release alleges that:

[F]rom at least October 2019 through January 2021, Costello and Ferraro engaged in a stock promotion scheme in which Ferraro recommended and promoted to his Twitter followers and the public at least five microcap stocks that Costello owned, without disclosing that he and Costello intended to sell shares of those stocks as their prices rose, or that Costello would pay Ferraro a portion of his profits from some of those sales. Costello shared approximately $32,000 of his profits with Ferraro, and Ferraro profited approximately $41,000 from his own trading in this scheme. The SEC's complaint also alleges that Ferraro separately conducted his own stock promotion scheme respecting two additional microcap stocks, generating profits of approximately $68,000.

Order Determining Whistleblower Award Claims ('34 Act Release No. 34-96232; Whistleblower Award Proc. File No. 2023-14)

https://www.sec.gov/rules/other/2022/34-96232.pdf

The SEC's Claims Review Staff ("CRS") issued a Preliminary Determination recommending the denial of a Whistleblower Award to Claimant 1 (seven Covered actions) and to Claimant 2. The Commission ordered that CRS's recommendations be approved. The Order asserts in part that [Ed: footnotes omitted]:

Because Claimant 1 obtained his/her information as a result of his/her association with the Company-which was retained to perform compliance functions-Claimant 1 must therefore satisfy at least one of Rule 21F-4(b)(4)(v)'s exceptions to receive an award. Claimant 1, however, has not done this.. . .We therefore conclude that Claimant 2 did not provide information that caused Staff to commence an examination, open or reopen an investigation, inquire concerning different conduct as part of a current examination or investigation that then resulted in the Commission bringing the Redacted Action, or significantly contribute to the success of the Redacted Action. . . .

SEC Awards Joint $1.6 Million Whistleblower Award to Three Claimant And A $1.6 Million Whistleblower Award to Fourth Claimant

Order Determining Whistleblower Award Claims ('34 Act Release No. 34-96231; Whistleblower Award Proc. File No. 2023-13)

https://www.sec.gov/rules/other/2022/34-96231.pdf

The SEC's Claims Review Staff ("CRS") issued a Preliminary Determination recommending the denial of a Whistleblower Award to Claimant. The Commission ordered that CRS's recommendations be approved. The Order asserts in part that [Ed: footnotes omitted]:

Claimant 4 requested reconsideration of the Preliminary Determinations asserting that (1) the information submitted by Claimants 1, 2, and 3 was not original information because it was based on information Claimant 4 submitted to Redacted ("Research Publication"), and (2) that the CRS overlooked several contributions made by Claimant 4 to the staff's investigation, as well as hardships Claimant 4 suffered, when determining the award percentage.. . .Contrary to Claimant 4's assertions in his/her reconsideration request, Claimants 1, 2, and 3 submitted original information in their Form TCR, which included information about *** Redacted . Claimants 1, 2, and 3's tip was submitted to the Commission before the Redacted Research Publication report and therefore, could not have been based on information contained in that report. . .. . .Furthermore, the additional contributions and hardships discussed in Claimant 4's request for reconsideration do not warrant a change in the award allocation. Most of the contributions cited by Claimant 4 concerned allegations that were not charged by the Commission. . . .

Order Determining Whistleblower Award Claims ('34 Act Release No. 34-96230; Whistleblower Award Proc. File No. 2023-12)

https://www.sec.gov/rules/other/2022/34-96230.pdf

The SEC's Claims Review Staff ("CRS") issued a Preliminary Determination recommending the denial of a Whistleblower Award to Claimant. The Commission ordered that CRS's recommendations be approved. The Order asserts in part that [Ed: footnotes omitted]:

The record also does not show that Claimant's information caused the staff to inquire into different conduct or significantly contributed to the ongoing Investigation. The staff declaration confirms that information in Claimant's TCR was already known to the staff, and Claimant's later conversations with the staff regarding Claimant's TCR, where Claimant provided additional documents, also did not yield any information not already known to the staff through its own investigation. Claimant also reported on the substance of a meeting Claimant had with an individual connected to the Defendants; however, Claimant's information about that meeting did not advance the Investigation or contribute to the success of the Covered Action as the staff was either already aware of the information or it was not relevant to the Investigation.Claimant's argument that Other Agency staff should be contacted because the Covered Action and the Other Agency actions are "deeply intertwined" is misplaced. As stated above, the initial question we examine is whether Claimant provided original information to the Commission that led to a successful Commission enforcement action.7 Commission staff are best-placed to determine Claimant's contributions to the Investigation and the Covered Action, and Claimant offers no plausible basis for why we should think otherwise. Based on the record, including the sworn declaration from Enforcement staff, which we credit, Claimant's information did not lead to the success of the Covered Action. We decline Claimant's invitation to gather additional information from Other Agency staff on the basis of Claimant's speculation that Other Agency staff may have more information about Claimant's contributions to the Commission Investigation and the Covered Action than Commission staff themselves.

Order Determining Whistleblower Award Claims ('34 Act Release No. 34-96229; Whistleblower Award Proc. File No. 2023-11)

https://www.sec.gov/rules/other/2022/34-96229.pdf

The SEC's Claims Review Staff ("CRS") issued a Preliminary Determination recommending the denial of a Whistleblower Award to Claimant. The Commission ordered that CRS's recommendations be approved. The Order asserts in part that [Ed: footnotes omitted]:

Claimant does not qualify for a whistleblower award on two independent grounds. First, Claimant did not submit Claimant's whistleblower application within the required ninety-day deadline. The requirement that claimants file whistleblower award claims within ninety days of the posting of a Notice of Covered Action ("NoCA"), set forth in Exchange Act Rule 21F-10, serves important programmatic functions. Here, Claimant's application was approximately seven months late. This ground alone renders Claimant ineligible for an award. Further, Claimant did not contest the CRS's recommended denial on this ground and accordingly forfeits Claimant's opportunity to contest on this ground.Claimant also does not qualify for an award on the ground that Claimant's information did not lead to the successful enforcement of the Covered Action. Enforcement staff confirms that the investigation that led to the Covered Action (the "Investigation") was opened based upon the staff's own investigative steps and not based on any information from Claimant. The staff also confirms that the staff did not receive any information provided by Claimant prior to opening the Investigation. Accordingly, Claimant's information did not cause the staff to open the Investigation.

Order Determining Whistleblower Award Claims ('34 Act Release No. 34-96228; Whistleblower Award Proc. File No. 2023-10)

https://www.sec.gov/rules/other/2022/34-96228.pdf

The SEC's Claims Review Staff ("CRS") issued a Preliminary Determination recommending the denial of a Whistleblower Award to Claimant. The Commission ordered that CRS's recommendations be approved. The Order asserts in part that [Ed: footnotes omitted]:

Here, Claimant's whistleblower application was submitted more than three months after the ninety-day filing period had closed. Claimant argues that the Commission should use its authority under Exchange Act Rule 21F-8(a) to waive the ninety-day filing requirement. Rule 21F-8(a) provides that "the Commission may, in its sole discretion, waive any of these procedures upon a showing of extraordinary circumstances." We have explained that the "extraordinary circumstances" exception is "narrowly construed" and requires an untimely claimant to show that "the reason for the failure to timely file was beyond the claimant's control." Further, we have identified "attorney misconduct or serious illness" that prevented a timely filing as two examples of the "demanding showing" that an applicant must make before we will consider exercising our discretionary authority to excuse an untimely filing.

Order Determining Whistleblower Award Claims ('34 Act Release No. 34-96227; Whistleblower Award Proc. File No. 2023-09)

https://www.sec.gov/rules/other/2022/34-96227.pdf

The SEC's Claims Review Staff ("CRS") issued a Preliminary Determination recommending the denial of a Whistleblower Award to Claimant. The Commission ordered that CRS's recommendations be approved. The Order asserts in part that [Ed: footnotes omitted]:

As an initial matter, Claimant first provided information to the staff in Redacted over four months after the staff opened the investigation that led to the Covered Action (the "Investigation") and more than one month after the Commission filed its complaint. Accordingly, Claimant cannot be credited with causing the staff to open an investigation.Second, the record does not demonstrate that Claimant significantly contributed to the success of the Covered Action or caused the staff to inquire into different conduct that was later the subject of a successful Commission enforcement action. Enforcement staff have confirmed, in a sworn supplemental declaration, which we credit, that Claimant's information did not advance the Investigation: Claimant's information related to the Individual who was not charged in the Covered Action. And the staff confirmed that it first became aware of the Individual in approximately Redacted about four months before Claimant provided information, and the Redacted staff was aware of the Individual's involvement with Redacted (the "Firm") the following month, approximately three months before Claimant submitted his information. The staff confirmed that Claimant's information was not a motivating factor in the decision to interview the Individual and that Claimant's information was either already known to the staff or did not advance the Investigation or contribute to the charges in the Covered Action. The staff also confirmed that Claimant's information did not assist the staff during settlement discussions with any of the Defendants.

In the Matter of Joel D. Plasco, Respondent (FINRA AWC 2020068211001)

https://www.finra.org/sites/default/files/fda_documents/2020068211001

%20Joel%20D.%20Plasco%20CRD%203220164%20AWC%20va.pdf

%20Joel%20D.%20Plasco%20CRD%203220164%20AWC%20va.pdf

For the purpose of proposing a settlement of rule violations alleged by the Financial Industry Regulatory Authority ("FINRA"), without admitting or denying the findings, prior to a regulatory hearing, and without an adjudication of any issue, Joel D. Plasco submitted a Letter of Acceptance, Waiver and Consent ("AWC"), which FINRA accepted. The AWC asserts that Joel D. Plasco entered the industry in 1999 and from October 2015 through November 2020, he was registered with Dalmore Group LLC. In accordance with the terms of the AWC, FINRA imposed upon Davis a $10,000 fine and a six-month suspension from associating with any FINRA member in all capacities. The AWC asserts in part that:

In April 2019, Plasco loaned $200,000 to a company for one month and expected to receive a 100 percent return at maturity. The loan was a security. After the company defaulted on the loan, the parties entered into a settlement agreement, pursuant to which Plasco received shares of a thinly-traded stock of a different company that he sold in a private transaction for $75,000. Plasco did not provide Dalmore Group with written notice or obtain the firm's written approval prior to participating in these private securities transactions. Therefore, Plasco violated FINRA Rules 3280 and 2010.. . .Between February 2020 and July 2020, Plasco opened outside brokerage accounts at three firms without the prior written consent of Dalmore Group. One of the firms held the account through which he effected the second private securities transaction described above. Therefore, Plasco violated FINRA Rules 3210 and 2010.. . .From 2016 until his departure from the firm in November 2020, Plasco served as a senior executive with and, in some instances, received compensation from six related businesses in the aviation industry. Plasco did not provide Dalmore Group with prior written notice of five of the six businesses and therefore violated FINRA Rules 3270 and 2010.